Tyson Foods 1999 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 1999 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

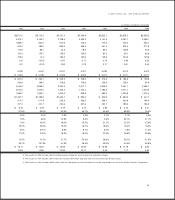

volume and dollars in millions, except per unit amounts

Weighted

average strike Fair

Volume price per unit value

As of Oct. 2, 1999

Recorded Balance Sheet Commodity Position:

Commodity inventory (book value of $33.8) — $««««««— $««33.8

Hedging Positions

Corn futures contracts (volume in bushels)

Long (buy) positions 84.4 2.21 (7.7)

Short (sell) positions 1.4 2.32 0.3

Soybean meal futures contracts (volume in tons)

Long (buy) positions 0.1 143.14 0.4

Trading Positions

Corn puts sold (volume in bushels) 27.5 2.10 (2.5)

As of Oct. 3, 1998

Recorded Balance Sheet Commodity Position:

Commodity inventory (book value of $36.0) — $««««««— $÷36.0

Hedging Positions

Corn futures contracts (volume in bushels)

Long (buy) positions 7.5 2.33 (0.4)

Short (sell) positions 9.7 2.11 0.3

Soybean oil futures contracts (volume in cwt)

Long (buy) positions 0.1 24.24 —

Short (sell) positions 0.1 24.40 —

Interest Rate and Foreign Currency Risks The Company hedges exposure to changes in interest rates on certain of its

financial instruments. Under the terms of various leveraged equipment loans, the Company enters into interest rate swap

agreements to effectively lock in a fixed interest rate for these borrowings. The maturity dates of these leveraged equip-

ment loans range from 2005 to 2008 with interest rates ranging from 4.7% to 6%.

The Company also periodically enters into foreign exchange forward contracts and option contracts to hedge some

of its foreign currency exposure. In 1999, the Company used such contracts to hedge exposure to changes in foreign cur-

rency exchange rates, primarily Mexican Peso, associated with debt denominated in U.S. dollars held by Tyson de

Mexico. In 1998, the Company used such contracts to hedge exposure to changes in foreign currency exchange rates,

primarily Japanese Yen, associated with sales denominated in foreign currency. Gains and losses on these contracts are

recognized as an adjustment of the subsequent transaction when it occurs. Forward and option contracts generally have

maturities or expirations not exceeding 12 months.

The following tables provide information about the Company’s derivative financial instruments and other financial

instruments that are sensitive to changes in interest rates. The tables present the Company’s debt obligations, principal

cash flows, related weighted-average interest rates by expected maturity dates and fair values. For interest rate swaps,

the tables present notional amounts, weighted-average interest rates or strike rates by contractual maturity dates and

fair values. Notional amounts are used to calculate the contractual cash flows to be exchanged under the contract.

Management’s discussion and analysis

TYSON FOODS, INC. 1999 ANNUAL REPORT

34