Toyota 2013 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2013 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Toyota Global Vision President’s Message Launching a New Structure Special Feature Review of Operations

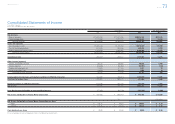

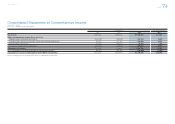

Consolidated Performance

Highlights

Management and

Corporate Information Investor InformationFinancial Section

Page 71

NextPrev

ContentsSearchPrint

ANNUAL REPORT 2013

Deferred Tax Assets

The factors used to assess the likelihood of realiza-

tion of the deferred tax assets are the future reversal

of existing taxable temporary differences, the future

taxable income and available tax planning strategies

that are prudent and feasible. All available evidence,

both positive and negative, is considered to deter-

mine whether, based on the weight of that evidence,

a valuation allowance is needed for deferred tax

assets which are not more-likely-than-not to

be realized.

The accounting for deferred tax assets represents

Toyota’s current best estimate based on all available

evidence. Unanticipated events or changes could

result in re-evaluating the realizability of deferred

tax assets.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Toyota is exposed to market risk from changes in

foreign currency exchange rates, interest rates, cer-

tain commodity and equity security prices. In order

to manage the risk arising from changes in foreign

currency exchange rates and interest rates, Toyota

enters into a variety of derivative fi nancial instruments.

A description of Toyota’s accounting policies for

derivative instruments is included in note 2 to the

consolidated fi nancial statements and further disclo-

sure is provided in notes 20 and 26 to the consoli-

dated fi nancial statements.

Toyota monitors and manages these fi nancial expo-

sures as an integral part of its overall risk management

program, which recognizes the unpredictability of

fi nancial markets and seeks to reduce the potential-

ly adverse effects on Toyota’s operating results.

The fi nancial instruments included in the market

risk analysis consist of all of Toyota’s cash and cash

equivalents, marketable securities, fi nance receiv-

ables, securities investments, long-term and short-

term debt and all derivative fi nancial instruments.

Toyota’s portfolio of derivative fi nancial instruments

Quantitative and Qualitative Disclosures about Market Risk

consists of forward foreign currency exchange con-

tracts, foreign currency options, interest rate swaps,

interest rate currency swap agreements and interest

rate options. Anticipated transactions denominated

in foreign currencies that are covered by Toyota’s

derivative hedging are not included in the market

risk analysis. Although operating leases are not

required to be included, Toyota has included these

instruments in determining interest rate risk.

Foreign Currency Exchange Rate Risk

Toyota has foreign currency exposures related to

buying, selling and fi nancing in currencies other

than the local currencies in which it operates.

Toyota is exposed to foreign currency risk related to

future earnings or assets and liabilities that are

exposed due to operating cash fl ows and various

fi nancial instruments that are denominated in foreign

currencies. Toyota’s most signifi cant foreign curren-

cy exposures relate to the U.S. dollar and the euro.

Toyota uses a value-at-risk analysis (“VAR”) to

evaluate its exposure to changes in foreign currency

exchange rates. The VAR of the combined foreign

exchange position represents a potential loss in pre-

tax earnings that was estimated to be ¥87.9 billion

and ¥99.1 billion at March 31, 2012 and 2013,

respectively. Based on Toyota’s overall currency

exposure (including derivative positions), the risk

during fi scal 2013 to pre-tax cash fl ow from curren-

cy movements was on average ¥99.1 billion, with a

high of ¥129.5 billion and a low of ¥78.1 billion.

The VAR was estimated by using a Monte Carlo

Simulation Method and assumed 95% confi dence level

on the realization date and a 10-day holding period.

Interest Rate Risk

Toyota is subject to market risk from exposures to

changes in interest rates based on its fi

nancing,

investing and cash management activities. Toyota

enters into various fi nancial instrument transactions

to maintain the desired level of exposure to the risk

of interest rate fl uctuations and to minimize interest

expense. The potential decrease in fair value result-

ing from a hypothetical 100 basis point upward shift

in interest rates would be approximately ¥144.2 bil-

lion as of March 31, 2012 and ¥208.5 billion as of

March 31, 2013.

There are certain shortcomings inherent to the

sensitivity analyses presented. The model assumes

that interest rate changes are instantaneous parallel

shifts in the yield curve. However, in reality, changes

are rarely instantaneous. Although certain assets

and liabilities may have similar maturities or periods

to repricing, they may not react correspondingly to

changes in market interest rates. Also, the interest

rates on certain types of assets and liabilities may

fl uctuate with changes in market interest rates,

while interest rates on other types of assets may lag

behind changes in market rates. Finance receiv-

ables are less susceptible to prepayments when

interest rates change and, as a result, Toyota’s

model does not address prepayment risk for auto-

motive related fi nance receivables. However, in the

event of a change in interest rates, actual loan pre-

payments may deviate signifi cantly from the

assumptions used in the model.

Commodity Price Risk

Commodity price risk is the possibility of higher or

lower costs due to changes in the prices of com-

modities, such as non-ferrous alloys (e.g., alumi-

num), precious metals (e.g., palladium, platinum and

rhodium) and ferrous alloys, which Toyota uses in

the production of motor vehicles. Toyota does not

use derivative instruments to hedge the price risk

associated with the purchase of those commodities

and controls its commodity price risk by holding

minimum stock levels.

Equity Price Risk

Toyota holds investments in various available-for-

sale equity securities that are subject to price risk.

The fair value of available-for-sale equity securities

was ¥1,034.3 billion as of March 31, 2012 and

¥1,401.1 billion as of March 31, 2013. The potential

change in the fair value of these investments,

assuming a 10% change in prices, would be

approximately ¥103.4 billion as of March 31, 2012

and ¥140.1 billion as of March 31, 2013.

Selected Financial Summary (U.S. GAAP) Consolidated Segment Information Consolidated Quarterly Financial Summary Management’s Discussion and Analysis of Financial Condition and Results of Operations [26 of 26] Consolidated Financial Statements Notes to Consolidated Financial Statements

Management’s Annual Report on Internal Control over Financial Reporting Report of Independent Registered Public Accounting Firm