TCF Bank 2012 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2012 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

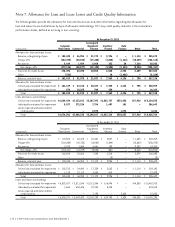

Loans and leases, including loans considered impaired,

are reviewed regularly by management. Consumer real estate

loans are placed on non-accrual status when the collection

of interest and principal is 150 days or more past due or

when six payments are owed. Consumer loans other than real

estate and auto loans are charged-off or written down to

collateral value less costs to sell at 120 days or more past

due or when five payments are owed. Consumer real estate

loans, consumer loans other than real estate, and auto

loans are generally placed on non-accrual status within

60 days of notification of bankruptcy, unless the customer

has a sustained period of payment performance of six months

or longer, including time prior to bankruptcy. Furthermore,

consumer real estate loans and consumer loans other than

real estate and auto loans, are permanently placed on non-

accrual status upon discharge under a Chapter 7 bankruptcy

proceeding when the borrower does not reaffirm the debt,

regardless of delinquency status.

Commercial real estate and commercial business

loans, leasing and equipment finance loans and leases and

inventory finance loans are generally placed on non-

accrual status when the collection of interest or principal

is 90 days or more past due, unless the loan or lease is

adequately collateralized and in the process of collection.

Generally, when a loan or lease is placed on non-

accrual status, uncollected interest accrued in prior years

is charged off against the allowance for loan and lease

losses and interest accrued in the current year is reversed

against interest income. For non-accrual leases that

have been funded on a non-recourse basis by third-party

financial institutions, the related liability is also placed on

non-accrual status. Interest payments received on loans

and leases in non-accrual status are generally applied to

principal unless the remaining principal balance has been

determined to be fully collectible, in which case interest

income is recognized on a cash basis. Loans on non-accrual

status are reported as non-accrual loans until there is

sustained repayment performance for six consecutive

months, with the exception of loans not reaffirmed upon

discharge under Chapter 7 bankruptcy, which remain on non-

accrual status permanently based upon regulatory guidance.

Income on these loans is recognized on a cash basis when

there is sustained repayment for six consecutive months

(which may include payments prior to bankruptcy), and the

loan is not more than 60 days delinquent.

Purchased Credit-Impaired (PCI) Loans acquired

with evidence of credit deterioration since their origination,

where it is probable TCF will not collect all contractually

required principal and interest payments, are recorded as

PCI loans. PCI loans are recorded at fair value at the date

of acquisition. Such loans are considered to be accruing

based on the existence of an accretable yield and not

based on consideration given to contractual interest

payments. The excess of expected cash flows to be

collected over the initial fair value of an acquired portfolio

is referred to as the accretable yield and is accreted into

interest income over the estimated life of the acquired

portfolios using the effective yield method. The difference

between the contractually required payments and the cash

flows expected to be collected at acquisition, considering

the impact of prepayments, is referred to as the non-

accretable difference.

Premises and Equipment Premises and equipment,

including leasehold improvements, are carried at cost and

are depreciated or amortized on a straight-line basis over

estimated useful lives of owned assets and for leasehold

improvements over the estimated useful life of the related

asset or the lease term, whichever is shorter. Maintenance

and repairs are charged to expense as incurred. Rent

expense for leased land with facilities is recognized in

occupancy and equipment expense. Rent expense for

leases with free rent periods or scheduled rent increases

is recognized on a straight-line basis over the lease term.

Other Real Estate Owned and Repossessed and

Returned Assets Assets acquired through foreclosure,

repossession or returned to TCF are initially recorded at

the lower of the loan or lease carrying amount or fair

value of the collateral less estimated selling costs at

the time of transfer to real estate owned or repossessed

and returned assets. The fair value of other real estate

owned is determined through independent third-party

appraisals, automated valuation methods or real estate

broker’s price opinions less estimated selling costs. The

fair value of repossessed and returned assets is based on

available pricing guides, auction results or price opinions

less estimated selling costs. Within 90 days or four months

of a loan or lease transferring to other real estate owned

or repossessed and returned assets, any carrying amount

in excess of the fair value less estimated selling costs is

charged off to the allowance for loan and lease losses.

Subsequently, if the fair value of an asset, less the

{ 2012 Form 10K } { 65 }