Starwood 2005 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2005 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

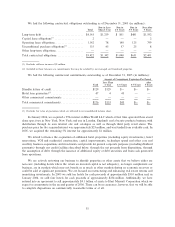

December 31, 2005, of which $8 million are expected to be funded in 2006 and $10 million are expected to be

funded in total. These loans typically are secured by pledges of project ownership interests and/or mortgages

on the projects. We also have $90 million of equity and other potential contributions associated with managed

or joint venture properties, $18 million of which is expected to be funded in 2006.

Additionally, during 2004, we entered into a long-term management contract to manage the Westin

Boston, Seaport Hotel in Boston, Massachusetts, which is under construction and scheduled to open in mid-

2006. In connection with this project, we agreed to provide up to $28 million in mezzanine loans and other

investments (all of which has been funded) as well as various guarantees, including a principal repayment

guarantee for the term of the senior debt (four years with a one-year extension option), which is capped at

$40 million, and a debt service guarantee during the term of the senior debt which is limited to the interest

expense on the amounts drawn under such debt and principal amortization. Any payments under the debt

service guarantee, attributable to principal, will reduce the cap under the principal repayment guarantee. The

fair value of these guarantees of $3 million is reÖected in other liabilities in our accompanying balance sheet as

of December 31, 2005. In addition, we have issued a completion guarantee for this approximate $200 million

project. In the event the completion guarantee is called on, we would have recourse to a guaranteed maximum

price contract from the general contractor, performance bonds from all major trade contractors and a payment

bond from the general contractor. We would only be required to perform under the completion guaranty in the

event of a default by the general contractor that is not cured by the contractor or the applicable bonds. We do

not anticipate that we will be required to perform under these guarantees.

Surety bonds issued on our behalf as of December 31, 2005 totaled $51 million, the majority of which

were required by state or local governments relating to our vacation ownership operations and by our insurers

to secure large deductible insurance programs.

To secure management contracts, we may provide performance guarantees to third-party owners. Most of

these performance guarantees allow us to terminate the contract rather than fund shortfalls if certain

performance levels are not met. In limited cases, we are obliged to fund shortfalls in performance levels

through the issuance of loans. As of December 31, 2005, we had six management contracts with performance

guarantees with possible cash outlays of up to $75 million, $50 million of which, if required, would be funded

over several years and would be largely oÅset by management fees received under these contracts. Many of the

performance tests are multi-year tests, are tied to the results of a competitive set of hotels, and have exclusions

for force majeure and acts of war and terrorism. We do not anticipate any signiÑcant funding under the

performance guarantees in 2006. In addition, we have agreed to guarantee certain performance levels at a

managed property that has authorized VOI sales and marketing. The exact amount and nature of the guaranty

is currently under dispute. However, we do not believe that any payments under this guaranty will be

signiÑcant. In connection with the acquisition of the Le Mπeridien brand in November 2005, we assumed the

obligation to guarantee certain performance levels at one Le Mπeridien managed hotel for the periods 2007

through 2013. This guarantee is uncapped, and we are still evaluating the potential impact. We do not

anticipate losing a signiÑcant number of management or franchise contracts in 2006.

In connection with the purchase of the Le Mπeridien brand in November 2005, we were indemniÑed for

certain of Le Mπeridien's historical liabilities by the entity that bought Le Mπeridien's owned and leased hotel

portfolio. The indemnity is limited to the Ñnancial resources of that entity. At this time, we believe that it is

unlikely that we will have to fund any of these liabilities.

34