Priceline 2011 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2011 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

86

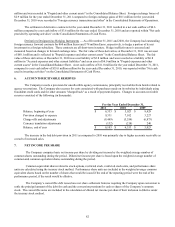

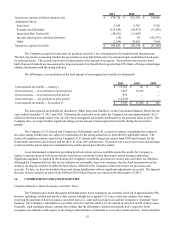

Convertible Debt

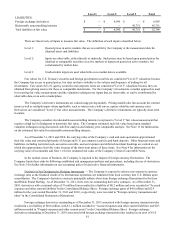

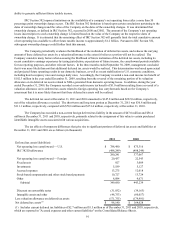

Convertible debt as of December 31, 2011 consists of the following (in thousands):

December 31, 2011

1.25% Convertible Senior Notes due March 2015

Outstanding

Principal

Amount

$ 575,000

Unamortized

Debt

Discount

$(77,360)

Carrying

Value

$ 497,640

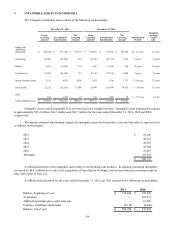

Convertible debt as of December 31, 2010 consisted of the following (in thousands):

December 31, 2010

1.25% Convertible Senior Notes due March 2015

0.75% Convertible Senior Notes due September 2013

Outstanding convertible debt

Outstanding

Principal

Amount

$ 575,000

213

$ 575,213

Unamortized

Debt

Discount

$(98,770)

(38)

$(98,808)

Carrying

Value

$ 476,230

175

$ 476,405

Based upon the closing price of the Company’s common stock for the prescribed measurement periods during the

three months ended December 31, 2011, the contingent conversion threshold of the 2015 Notes was exceeded. Therefore, the

2015 Notes are convertible at the option of the holders. Accordingly, the Company reported the carrying value of the 2015

Notes as a current liability as of December 31, 2011. Since these notes are convertible at the option of the holders and the

principal amount is required to be paid in cash, the difference between the principal amount and the carrying value is reflected

as convertible debt in the mezzanine section on the Company's Consolidated Balance Sheet. Therefore, with respect to the

2015 Notes, the Company reclassified $77.4 million before tax from additional paid-in-capital to convertible debt in the

mezzanine section on the Company's Consolidated Balance Sheet. The contingent conversion threshold on the 2015 Notes was

not exceeded at December 31, 2010, and therefore on that date the debt was reported as a non-current liability. The

determination of whether or not the 2015 Notes are convertible must continue to be performed on a quarterly basis.

Consequently, the 2015 Notes may not be convertible in future quarters, and therefore may again be classified as long-term

debt, if the contingent conversion threshold is not met in such quarters.

Based upon the closing price of the Company's common stock for the prescribed measurement period during the three

months ended December 31, 2010, the contingent consideration threshold on the 2013 Notes was exceeded. As a result, the

2013 Notes were convertible at the option of the holders as of December 31, 2010, and accordingly were classified as a current

liability as of that date. The remaining outstanding principal amount of the 2013 Notes was converted during the three months

ended June 30, 2011.

If the note holders exercise their option to convert, the Company delivers cash to repay the principal amount of the

notes and delivers shares of common stock or cash, at its option, to satisfy the conversion value in excess of the principal

amount. In cases where holders decide to convert prior to the maturity date, the Company writes off the proportionate amount

of remaining debt issuance costs to interest expense. In the year ended December 31, 2011, the Company delivered cash of

$0.2 million to repay the principal amount and issued 4,869 shares of its common stock in satisfaction of the conversion value

in excess of the principal amount for convertible debt that was converted prior to maturity. The Company delivered cash of

$195.6 million to repay the principal amount, and issued 3,457,828 shares of its common stock and delivered $99.8 million in

cash in satisfaction of the conversion value in excess of the principal amount for convertible debt converted prior to maturity

for the year ended December 31, 2010.

As of December 31, 2011 and 2010, the estimated market value of the outstanding senior notes was approximately

$0.9 billion for both periods. Fair value was estimated based upon actual trades at the end of the reporting period or the most

recent trade available as well as the Company’s stock price at the end of the reporting period. A substantial portion of the

market value of the Company’s debt in excess of the outstanding principal amount relates to the conversion premium on the

bonds.