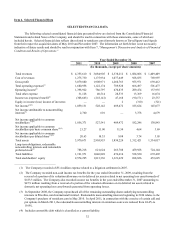

Priceline 2011 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2011 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

36

While demand for online travel services in the U.S. continues to experience annualized growth, we believe that the

domestic market share of third-party distributors is impacted in part by a concerted initiative by travel suppliers to direct

customers to their own websites in an effort to reduce distribution expenses and establish more direct control over their pricing.

The launch of Room Key discussed above is demonstrative of such efforts. In addition, certain suppliers have attempted to

charge additional fees to customers who book airline reservations through an online channel other than their own website.

Suppliers who sell on their own websites typically do not charge a processing fee, and, in some instances, offer advantages

such as web-only fares, bonus miles or loyalty points, which could make their offerings more attractive to consumers than

models like ours.

Some travel suppliers are encouraging third-party travel intermediaries, such as us, to develop technology to bypass

the traditional GDSs, such as enabling direct connections to the travel suppliers or using alternative global distribution

methods. For example, in 2011, we enabled a direct connection with American Airlines. During 2011, American Airlines

content was temporarily unavailable on Expedia and Orbitz due to disputes related to enabling a direct connection. We believe

that this is consistent with an effort on the part of American Airlines, and the airline industry in general, to reduce distribution

costs and could be indicative of the airlines in general becoming more aggressive in requiring online travel agents to implement

direct connections. Development and implementation of the technology to enable additional direct connections to travel

suppliers could cause us to incur additional operating expenses, increase the frequency/duration of system problems and delay

other projects. In addition, any additional migration toward direct connections would reduce the compensation we receive from

GDSs.

Domestic airlines have reduced capacity and increased fares since the latter part of 2009, a trend which may continue.

Decreases in capacity reduce the amount of airline tickets available, while significant increases in average airfares over the last

two years have adversely impacted leisure travel demand. Reduced airline capacity and demand negatively impact our

priceline.com air business, which in turn has negative repercussions on our priceline.com hotel and rental car businesses. Our

rental car business is further impacted by decreases in rental car fleets, which has negatively impacted our Name Your Own

Price® rental car service. We expect continued variability in the breadth and depth of discounted airline tickets and rental car

rates made available to us in the future, depending on market conditions from time to time.

Seasonality. A meaningful amount of retail gross bookings are generated early in the year, as customers plan and

reserve their spring and summer vacations in Europe and North America. However, we do not recognize associated revenue

until future quarters when the travel occurs. From a cost perspective, we expense the substantial majority of our advertising

activities as they are incurred, which is typically in the quarter in which bookings are generated. As a result, we typically

experience our highest levels of profitability in the second and third quarters of the year, which is when we experience the

highest levels of booking and travel consumption for the year for our North American and European businesses. However, we

experience the highest levels of booking and travel consumption for our Asia-Pacific and South American businesses in the first

and fourth quarters. Therefore, if these businesses continue to grow faster than our North American and European businesses,

our operating results for the first and fourth quarters of the year may become more significant over time as a percentage of full

year operating results. In addition, Our Name Your Own Price® services are generally non-refundable in nature, and

accordingly, we recognize travel revenue at the time a booking is generated. However, we recognize revenue generated from

our retail hotel services, including Booking.com and Agoda, at the time that the customer checks out of the hotel. Therefore, if

our retail hotel business continues to grow, we expect our quarterly results to become increasingly impacted by these seasonal

factors.

Other Factors. We believe that our success will depend in large part on our ability to maintain profitability, primarily

from our hotel business, to continue to promote the Booking.com, Agoda and rentalcars.com brands internationally and the

priceline.com brand in the United States, and, over time, to offer other travel services and further expand into other

international markets. Factors beyond our control, such as worldwide recession, higher oil prices, terrorist attacks, unusual

weather patterns, natural disasters such as earthquakes, hurricanes, tsunamis, floods, volcanic eruptions (such as the April 2010

eruption of a volcano in Iceland), travel related health concerns including pandemics and epidemics such as Influenza H1N1,

avian bird flu and SARS, political instability, regional hostilities, imposition of taxes or surcharges by regulatory authorities,

travel related accidents or the withdrawal from our system of a major hotel supplier or airline, could adversely affect our

business and results of operations and impair our ability to effectively implement all or some of the initiatives described above.

For example, in early 2011, Japan was struck by a major earthquake, tsunami and nuclear emergency. Japan is an

important source of travel demand for Agoda, and these crises have had an adverse impact on travel demand originating in

Japan and demand for Japanese destinations. In October 2011, severe flooding in Thailand, a key market for our Agoda

business and the Asian business of Booking.com, negatively impacted booking volumes and cancellation rates in this market.

In addition, in early 2010, Thailand experienced disruptive civil unrest, which caused the temporary relocation of Agoda's

Thailand-based operations. Future natural disasters or civil or political unrest could further disrupt our business and operations