Priceline 2011 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2011 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

81

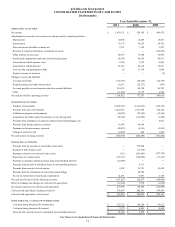

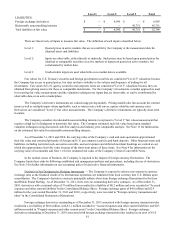

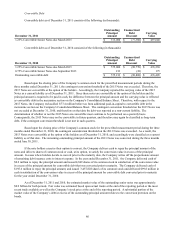

LIABILITIES:

Foreign exchange derivatives

Redeemable noncontrolling interests

Total liabilities at fair value

Level 1

$ —

—

$ —

Level 2

$ 6,995

—

$ 6,995

Level 3

$ —

45,751

$ 45,751

Total

$ 6,995

45,751

$ 52,746

There are three levels of inputs to measure fair value. The definition of each input is described below:

Level 1: Quoted prices in active markets that are accessible by the Company at the measurement date for

identical assets and liabilities.

Level 2: Inputs are observable, either directly or indirectly. Such prices may be based upon quoted prices for

identical or comparable securities in active markets or inputs not quoted on active markets, but

corroborated by market data.

Level 3: Unobservable inputs are used when little or no market data is available.

Fair values for U.S. Treasury securities and foreign government securities are considered "Level 2" valuations because

the Company has access to quoted prices, but does not have visibility to the volume and frequency of trading for all

investments. Fair values for U.S. agency securities and corporate notes are considered "Level 2" valuations because they are

obtained from pricing sources for these or comparable instruments. For the Company’s investments, a market approach is used

for recurring fair value measurements and the valuation techniques use inputs that are observable, or can be corroborated by

observable data, in an active marketplace.

The Company’s derivative instruments are valued using pricing models. Pricing models take into account the contract

terms as well as multiple inputs where applicable, such as interest rate yield curves, option volatility and currency rates.

Derivatives are considered "Level 2" fair value measurements. The Company’s derivative instruments are typically short-term

in nature.

The Company considers its redeemable noncontrolling interests to represent a "Level 3" fair value measurement that

requires a high level of judgment to determine fair value. The Company estimated such fair value based upon standard

valuation techniques using discounted cash flow analysis and industry peer comparable analysis. See Note 13 for information

on the estimated fair value for redeemable noncontrolling interests.

As of December 31, 2011 and 2010, the carrying value of the Company’s cash and cash equivalents approximated

their fair value and consisted primarily of foreign and U.S. government securities and bank deposits. Other financial assets and

liabilities, including restricted cash, accounts receivable, accrued expenses and deferred merchant bookings are carried at cost

which also approximates their fair value because of the short-term nature of these items. See Note 4 for information on the

carrying value of investments and Note 11 for the estimated fair value of the Company’s Senior Convertible Notes.

In the normal course of business, the Company is exposed to the impact of foreign currency fluctuations. The

Company limits these risks by following established risk management policies and procedures, including the use of derivatives.

See Note 2 for further information on our accounting policy for derivative financial instruments.

Derivatives Not Designated as Hedging Instruments — The Company is exposed to adverse movements in currency

exchange rates as the financial results of its international operations are translated from local currency into U.S. Dollars upon

consolidation. The Company's derivative contracts principally address short-term foreign exchange fluctuations for the Euro

and British Pound Sterling. As of December 31, 2011, there were no outstanding derivative contracts. As of December 31,

2010, derivatives with a notional value of 30 million Euros resulted in a liability of $0.2 million and were recorded in "Accrued

expenses and other current liabilities"in the Consolidated Balance Sheet. Foreign exchange gains of $4.0 million and $2.9

million for the years ended December 31, 2011 and 2010 , respectively, were recorded in "Foreign currency transactions and

other" in the Consolidated Statements of Operations.

Foreign exchange derivatives outstanding as of December 31, 2011 associated with foreign currency transaction risks

resulted in a net liability of $0.8 million, with $1.1 million recorded in "Accrued expenses and other current liabilities and $0.3

million recorded in "Prepaid expenses and other current assets" in the Consolidated Balance Sheet. Foreign exchange

derivatives outstanding at December 31, 2010 associated with foreign exchange transaction risks resulted in an asset of $1.0