Priceline 2011 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2011 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

76

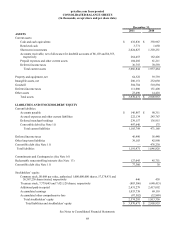

subsidiary’s net assets. Gains and losses are recognized on the Consolidated Balance Sheet in "Accumulated other

comprehensive loss" and will be realized upon a partial sale or liquidation of the investment. The Company formally

documents all derivatives designated as hedging instruments for accounting purposes, both at hedge inception and on an on-

going basis. These net investment hedges expose the Company to liquidity risk as the derivatives have an immediate cash flow

impact upon maturity, which is not offset by the translation of the underlying hedged equity. The cash flows from these

contracts are classified within "Net cash used in investing activities" on the cash flow statement.

The Company does not use financial instruments for trading or speculative purposes. The Company recognizes all

derivative instruments on the balance sheet at fair value and its derivative instruments are generally short-term in duration. The

derivative instruments do not contain leverage features.

The Company is exposed to the risk that counterparties to derivative contracts may fail to meet their contractual

obligations. The Company regularly reviews its credit exposure as well as assessing the creditworthiness of its counterparties.

See Note 5 for further detail on derivatives.

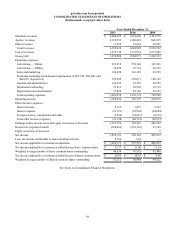

Recent Accounting Pronouncements

In December 2011, the Financial Accounting Standards Board ("FASB") issued guidance for new disclosure

requirements regarding a company's rights of offset and related arrangements associated with financial instruments and

derivative instruments. The new disclosures are designed to make financial statements that were prepared under U.S. GAAP

more comparable to those prepared under International Financial Reporting Standards ("IFRS"). The new disclosure

requirements are effective for annual reporting periods beginning on or after January 1, 2013, and interim periods therein.

Retrospective application is required.

In September 2011, the FASB issued an accounting update, which amends the guidance on testing goodwill for

impairment. Under the revised guidance, entities testing goodwill for impairment have the option of performing a qualitative

assessment before calculating the fair value of the reporting unit. If, based on the qualitative factors, it is more-likely-than not

that the fair value of the reporting unit is less than its carrying value, then the unchanged two-step approach previously used

would be required. The new accounting guidance does not change how goodwill is calculated, how goodwill is assigned to the

reporting unit, or the requirements for testing goodwill annually or when events and circumstances warrant testing. The

accounting update is effective for annual and interim periods beginning after December 15, 2011. Early adoption of the update

is permitted. During the three months ended September 30, 2011, the Company performed its annual quantitative goodwill

impairment testing, and concluded that the estimated fair value for each reporting unit substantially exceeds its respective

carrying value. This new accounting guidance will not have a significant impact on the Company.

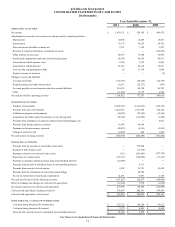

In June 2010, the FASB issued amended accounting guidance on the presentation of other comprehensive income in

financial statements by requiring comprehensive income to be reported in either a single statement or in two consecutive

statements reporting net income and other comprehensive income. This accounting update also required reclassification

adjustments out of other comprehensive income to be presented in both the income statement and the statement in which other

comprehensive income is presented, both in interim and annual periods. In December 2011, the FASB issued another

accounting update which indefinitely defers the requirement to separately present reclassification adjustments on the face of

the financial statements. During the deferral period, a company that does not display reclassification adjustments on the face of

the financial statements must disclose such adjustments in the notes to the financial statements. The accounting guidance did

not change the items that constitute net income or other comprehensive income, the timing of when other comprehensive

income is reclassified to net income, or the earnings per share computation. The accounting update requires retrospective

application. Public entities will be required to adopt the guidance for fiscal years, and interim periods within those years,

beginning after December 15, 2011, with early adoption permitted. The Company will comply with the change in presentation

of other comprehensive income in the financial statements beginning in the first quarter of 2012.

In May 2010, the FASB issued amended guidance on fair value to largely achieve common fair value measurement

and disclosure requirements between U.S. GAAP and IFRS. The new accounting guidance does not extend the use of fair

value but rather provides guidance about how fair value should be determined. For U.S. GAAP, most of the changes are

clarifications of existing guidance or wording changes to align with IFRS. Amendments that clarify the Board's intent under

existing requirements include: (a) use of the highest and best use and valuation premise concept should be limited to

nonfinancial assets; (b) disclosure should include quantitative information about the unobservable inputs used in a fair value

measurement that is categorized within Level 3 of the fair value hierarchy; and (c) the fair value of an instrument classified in

an entity's equity should be valued from the perspective of a market participant that holds that instrument as an asset. The

amended guidance changes requirements as follows: (a) disclosures are expanded, particularly those relating to fair value

measurements based on unobservable inputs, (b) fair value measurements for financial assets and liabilities based on a net