Priceline 2011 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2011 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

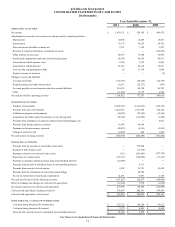

75

Income Taxes — The Company accounts for income taxes under the asset and liability method. The Company records

the estimated future tax effects of temporary differences between the tax bases of assets and liabilities and amounts reported on

the Consolidated Balance Sheets, as well as operating loss and tax credit carryforwards. Deferred taxes are classified as current

or noncurrent based on the balance sheet classification of the related assets and liabilities.

The Company records deferred tax assets to the extent it believes these assets will more likely than not be realized.

The Company regularly reviews its deferred tax assets for recoverability considering historical profitability, projected future

taxable income, the expected timing of the reversals of existing temporary differences, the carryforward periods available for

tax reporting purposes, and tax planning strategies. A valuation allowance is provided when it is more likely than not that some

portion or all of a deferred tax asset will not be realized. The ultimate realization of deferred tax assets depends on the

generation of future taxable income during the period in which related temporary differences become deductible. In

determining the future tax consequences of events that have been recognized in the financial statements or tax returns,

significant judgments, estimates, and interpretation of statutes are required.

Deferred taxes are measured using the enacted tax rates expected to apply to taxable income in the years in which

those temporary differences are expected to be recovered or settled. The effect on deferred taxes of a change in tax rates is

recognized in income in the period that includes the enactment date of such change.

Income taxes are not accrued for unremitted earnings of international operations that have been or are intended to be

reinvested indefinitely.

The Company recognizes liabilities when it believes that uncertain positions may not be fully sustained upon review

by the tax authorities. Liabilities recognized for uncertain tax positions are based on a two step approach for recognition and

measurement. First, the Company evaluates the tax position for recognition by determining if the weight of available evidence

indicates it is more likely than not that the position will be sustained on audit based on its technical merits. Secondly, the

Company measures the tax benefit as the largest amount which is more than 50% likely of being realized upon ultimate

settlement. Interest and penalties attributable to uncertain tax positions, if any, are recognized as a component of income tax

expense. See Note 15 for further details on income taxes.

Segment Reporting — The Company operates and manages its business as a single reportable unit. Operating

segments that have similar economic characteristics are aggregated. For geographic related information, see Note 18 to the

Company’s Consolidated Financial Statements.

Foreign Currency Translation — The functional currency of the Company’s foreign subsidiaries is generally their

respective local currency. Assets and liabilities are translated into U.S. dollars at the rate of exchange existing at the balance

sheet date. Income statement amounts are translated at average monthly exchange rates applicable for the period. Translation

gains and losses are included as a component of "Accumulated other comprehensive loss" on the Company’s Consolidated

Balance Sheets. Foreign currency transaction gains and losses are included in "Foreign currency transactions and other" in the

Company’s Consolidated Statements of Operations.

Derivative Financial Instruments — As a result of the Company’s international operations, it is exposed to various

market risks that may affect its consolidated results of operations, cash flow and financial position. These market risks include,

but are not limited to, fluctuations in currency exchange rates. The Company’s primary foreign currency exposures are in

Euros and British Pound Sterling, in which it conducts a significant portion of its business activities. As a result, the Company

faces exposure to adverse movements in currency exchange rates as the financial results of its international operations are

translated from local currency into U.S. Dollars upon consolidation. Additionally, foreign exchange rate fluctuations on

transactions denominated in currencies other than the functional currency result in gains and losses that are reflected in income.

The Company may enter into derivative instruments to hedge certain net exposures of nonfunctional currency

denominated assets and liabilities and the volatility associated with translating foreign earnings into U.S. Dollars, even though

it does not elect to apply hedge accounting or hedge accounting does not apply. Gains and losses resulting from a change in

fair value for these derivatives are reflected in income in the period in which the change occurs and are recognized on the

Consolidated Statements of Operations in "Foreign currency transactions and other." Cash flows related to these contracts are

classified within "Net cash provided by operating activities" on the cash flow statement.

The Company also utilizes derivative instruments to hedge the impact of changes in currency exchange rates on the

net assets of its foreign subsidiaries. These instruments are designated as net investment hedges. Hedge ineffectiveness is

assessed and measured based on changes in forward exchange rates. The Company records gains and losses on these derivative

instruments as currency translation adjustments, which offset a portion of the translation adjustments related to the foreign