Pep Boys 2008 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2008 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

‘‘Accounting for Uncertainty in Income Taxes’’ (‘‘FIN 48’’). FIN 48 clarifies the accounting for

uncertainty in income taxes recognized in an enterprise’s financial statements and prescribes a

recognition threshold and measurement attributes of income tax positions taken or expected to

be taken on a tax return. Under FIN 48, the impact of an uncertain tax position taken or

expected to be taken on an income tax return must be recognized in the financial statements at

the largest amount that is more-likely-than-not to be sustained. An uncertain income tax position

will not be recognized in the financial statements unless it is more-likely-than-not to be

sustained. We adjust these tax liabilities, as well as the related interest and penalties, based on

the latest facts and circumstances, including recently published rulings, court cases, and

outcomes of tax audits. To the extent our actual tax liability differs from our established tax

liabilities for unrecognized tax benefits, our effective tax rate may be materially impacted. While

it is often difficult to predict the final outcome of, the timing of, or the tax treatment of any

particular tax position or deduction, we believe that our tax balances reflect the

more-likely-than-not outcome of known tax contingencies.

The temporary differences between the book and tax treatment of income and expenses result in

deferred tax assets and liabilities, which are included within our consolidated balance sheets. We

must then assess the likelihood that our deferred tax assets will be recovered from future taxable

income. To the extent we believe that recovery is not more likely than not, we must establish a

valuation allowance. In this regard when determining whether or not we should establish a

valuation allowance, the Company considers various tax planning strategies, including potential

real estate transactions, as future taxable income. To the extent we establish a valuation

allowance or change the allowance in a future period, income tax expense will be impacted.

Actual results could differ from this assessment if adequate taxable income is not generated in

future periods from either operations or projected tax planning strategies. We had net deferred

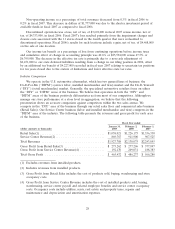

tax assets of $41,860,000 and $32,612,000 as of January 31, 2009 and February 2, 2008,

respectively.

RECENT ACCOUNTING STANDARDS

The Company adopted the provisions of FIN 48 on February 4, 2007. In connection with the

adoption, the Company recorded a net decrease to retained earnings of $155,000 and reclassified

certain previously recognized deferred tax attributes as FIN 48 liabilities. For additional information,

see Note 14, ‘‘Income Taxes.’’

In September 2006, the FASB issued SFAS No. 158, ‘‘Employers’ Accounting for Defined Benefit

Pension and Other Postretirement Plans—an Amendment of FASB Statements No. 87, 88, 106 and

132(R)’’ (SFAS 158). SFAS No. 158 requires entities to:

• Recognize on its balance sheet the funded status (measured as the difference between the fair

value of plan assets and the benefit obligation) of pension and other postretirement benefit

plans;

• Recognize, through comprehensive income, certain changes in the funded status of a defined

benefit and post retirement plan in the year in which the changes occur;

• Measure plan assets and benefit obligations as of the end of the employer’s fiscal year; and

• Disclose additional information.

The Company adopted the requirement to recognize the funded status of a benefit plan and the

additional disclosure requirements at February 3, 2007. At February 2, 2008, the Company adopted the

SFAS No. 158 requirement to measure plan assets and benefit obligations as of the date of the

Company’s fiscal year end. In accordance with SFAS 158, the change of measurement date from a

calendar year to the Company’s fiscal year resulted in a net charge to Retained Earnings of $189,000

31