Pep Boys 2008 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2008 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

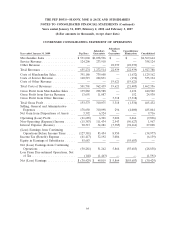

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 31, 2009, February 2, 2008 and February 3, 2007

(dollar amounts in thousands, except share data)

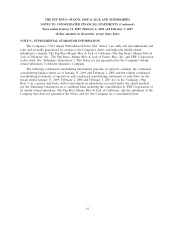

NOTE 10—BENEFIT PLANS

DEFINED BENEFIT PLANS

The Company has a defined benefit pension plan covering substantially all of its full-time

employees hired on or before February 1, 1992. Normal retirement age is 65. Pension benefits are

based on salary and years of service. The Company’s policy is to fund amounts as are necessary on an

actuarial basis to provide assets sufficient to meet the benefits to be paid to plan members in

accordance with the requirements of ERISA.

The actuarial computations are made using the ‘‘projected unit credit method.’’ Variances between

actual experience and assumptions for costs and returns on assets are amortized over the remaining

service lives of employees under the plan.

As of December 31, 1996, the Company froze the accrued benefits under the plan and active

participants became fully vested. The plan’s trustee will continue to maintain and invest plan assets and

will administer benefit payments.

The Company also has a Supplemental Executive Retirement Plan (SERP). This unfunded plan

has a defined benefit component that provides key employees designated by the Board of Directors

with retirement and death benefits. Retirement benefits are based on salary and bonuses; death

benefits are based on salary. Benefits paid to a participant under the defined pension plan are

deducted from the benefits otherwise payable under the defined benefit portion of the SERP. On

January 31, 2004, we amended and restated our SERP. This amendment converted the defined benefit

portion of the SERP to a defined contribution portion for certain unvested participants and all future

participants. On December 31, 2008 the Company terminated the defined benefit portion of the SERP

with a $14,441 payment and recorded a $6,005 settlement charge in accordance with SFAS No.88

‘‘Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for

Termination Benefits.’’

The Company uses a fiscal-end measurement date for determining benefit obligations and the fair

value of plan assets of its plans.

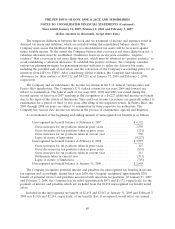

Pension expense includes the following:

Year ended

January 31, February 2, February 3,

2009 2008 2007

Service cost ......................................... $ 110 $ 166 $ 246

Interest cost ......................................... 3,346 3,419 3,071

Expected return on plan assets ........................... (2,450) (2,320) (2,176)

Amortization of transitional obligation ...................... 150 163 163

Amortization of prior service cost ......................... 340 370 360

Recognized actuarial loss ............................... 975 1,814 2,335

Net periodic benefit cost ................................ 2,471 3,612 3,999

Settlement charge .................................... 6,005 — —

Total Pension Expense ................................. $8,476 $ 3,612 $ 3,999

70