Pep Boys 2008 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2008 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

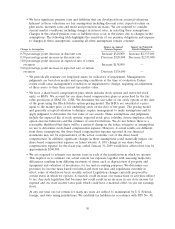

• We have significant pension costs and liabilities that are developed from actuarial valuations.

Inherent in these valuations are key assumptions including discount rates, expected return on

plan assets, mortality rates and merit and promotion increases. We are required to consider

current market conditions, including changes in interest rates, in selecting these assumptions.

Changes in the related pension costs or liabilities may occur in the future due to changes in the

assumptions. The following table highlights the sensitivity of our pension obligations and expense

to changes in these assumptions, assuming all other assumptions remain constant:

Impact on Annual Impact on Projected

Change in Assumption Pension Expense Benefit Obligation

0.50 percentage point decrease in discount rate ......... Increase $320,000 Increase $2,335,000

0.50 percentage point increase in discount rate .......... Decrease $320,000 Decrease $2,335,000

5.00 percentage point decrease in expected rate of return

on assets ................................... Increase $138,000 —

5.00 percentage point increase in expected rate of return

on assets ................................... Decrease $138,000 —

• We periodically evaluate our long-lived assets for indicators of impairment. Management’s

judgments are based on market and operating conditions at the time of evaluation. Future

events could cause management’s conclusion on impairment to change, requiring an adjustment

of these assets to their then current fair market value.

• We have a share-based compensation plan, which includes stock options and restricted stock

units, or RSUs. We account for our share-based compensation plans as prescribed by the fair

value provisions of SFAS No. 123R. We determine the fair value of our stock options at the date

of the grant using the Black-Scholes option-pricing model. The RSUs are awarded at a price

equal to the market price of our underlying stock on the date of the grant. The pricing model

and generally accepted valuation techniques require management to make assumptions and to

apply judgment to determine the fair value of our awards. These assumptions and judgments

include the expected life of stock options, expected stock price volatility, future employee stock

option exercise behaviors and the estimate of award forfeitures. We do not believe there is a

reasonable likelihood that there will be a material change in the future estimates or assumptions

we use to determine stock-based compensation expense. However, if actual results are different

from these assumptions, the share-based compensation expense reported in our financial

statements may not be representative of the actual economic cost of the share-based

compensation. In addition, significant changes in these assumptions could materially impact our

share-based compensation expense on future awards. A 10% change in our share-based

compensation expense for the fiscal year ended January 31, 2009 would have affected net loss by

approximately $200,000.

• We are required to estimate our income taxes in each of the jurisdictions in which we operate.

This requires us to estimate our actual current tax exposure together with assessing temporary

differences resulting from differing treatment of items, such as depreciation of property and

equipment and valuation of inventories, for tax and accounting purposes. We determine our

provision for income taxes based on federal and state tax laws and regulations currently in

effect, some of which have been recently revised. Legislation changes currently proposed by

certain states in which we operate, if enacted, could increase our transactions or activities subject

to tax. Any such legislation that becomes law could result in an increase in our state income tax

expense and our state income taxes paid, which could have a material effect on our net earnings

(loss).

At any one time our tax returns for many tax years are subject to examination by U.S. Federal,

foreign, and state taxing jurisdictions. We establish tax liabilities in accordance with FIN No. 48,

30