Nordstrom 2013 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2013 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

30

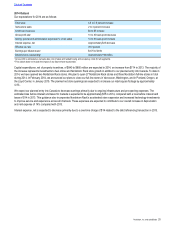

In November 2013, our wholly owned subsidiary in Puerto Rico entered into a $52 unsecured borrowing facility that expires in November

2018 to support our expansion into that market. We borrowed $2 against this facility during 2013.

We have a registration statement on file with the Securities and Exchange Commission using a “shelf” registration process. Under this shelf

registration process, we may offer and sell, from time to time, any combination of the securities described in a prospectus to the registration

statement, including registered debt, provided we maintain Well-known Seasoned Issuer (“WKSI”) status.

We maintain trade and standby letters of credit to facilitate international payments. As of February 1, 2014, we have $8 available under a

trade letter of credit, with $3 outstanding, and $15 available under the standby letter of credit, with $2 outstanding at the end of the year.

As of February 1, 2014, we had approximately $125 of fee interest in our Manhattan full-line store subject to lien. We have committed to

make future installment payments based on the developer of the property meeting construction and development milestones. Our fee interest

in the property is subject to lien until project completion or fulfillment of our existing installment payment commitment.

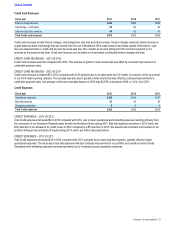

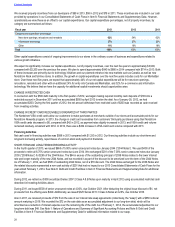

Impact of Credit Ratings

Under the terms of our revolver, any borrowings we may enter into will accrue interest for Euro-Dollar Rate Loans at a floating base rate tied

to LIBOR, for Canadian Dealer Offer Rate Loans at a floating rate tied to CDOR, and for Base Rate Loans at the highest of: (i) the Euro-

Dollar rate plus 100 basis points, (ii) the federal funds rate plus 50 basis points and (iii) the prime rate.

The rate depends upon the type of borrowing incurred, plus in each case an applicable margin. This applicable margin varies depending

upon the credit ratings assigned to our long-term unsecured debt. At the time of this report, our long-term unsecured debt ratings, outlook

and resulting applicable margin were as follows:

Credit Ratings Outlook

Moody’s Baa1 Stable

Standard & Poor’s A- Stable

Base Interest

Rate Applicable

Margin

Euro-Dollar Rate Loan LIBOR 0.9%

Canadian Dealer Offer Rate Loan CDOR 0.9%

Base Rate Loan various —

Should the ratings assigned to our long-term unsecured debt improve, the applicable margin associated with any such borrowings may

decrease, resulting in a slightly lower borrowing cost under this facility. Should the ratings assigned to our long-term unsecured debt worsen,

the applicable margin associated with our borrowings may increase, resulting in a slightly higher borrowing cost under this facility.

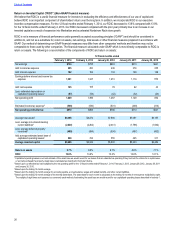

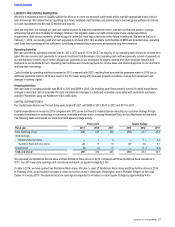

Debt Covenants

The new revolver requires that we maintain an adjusted debt to earnings before interest, income taxes, depreciation, amortization and rent

(“EBITDAR”) leverage ratio of less than four times (see the following additional discussion of Adjusted Debt to EBITDAR).

As of February 1, 2014 and February 2, 2013, we were in compliance with this covenant. We will continue to monitor this covenant and

believe that we will remain in compliance with this covenant during 2014.

Table of Contents