Nissan 2008 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2008 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

5

Nissan Annual Report 2008

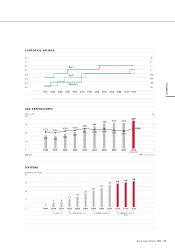

We are countering foreign exchange rate

fluctuations by manufacturing where we sell

whenever possible, since the best way to hedge is to

keep your costs in the same currency as your

revenues. That also reduces logistics-related

expenses and custom duties, which are very

significant for an international company like Nissan.

Developing our manufacturing facilities in Russia,

China and India also serves the same purpose.

Sharing investments costs with our Alliance

partner optimizes capital expenditures. Renault is

investing in Morocco, for example, and we benefit.

We are investing in Mexico, to Renault’s benefit.

Now, we are sharing capacity, engineering, and

development on the Alliance ultra-low-cost car in a

new country for both of us—India. This reduces

capital expenditures, which makes both companies

leaner and more efficient.

Investors putting their money into Nissan

appreciate our dividend policy. As we announced, our

2008 dividend will be 42 yen per share. We are also

taking care of our other stakeholders—customers,

employees, and suppliers. Safeguarding the

environment is another priority, and why we are

focusing strongly on electric vehicles, sharing related

investment and research and development costs with

Renault.

The liquidity risk is probably the most dangerous

one of all. Today, it’s even more pronounced, and it

can quickly become a factor that determines survival.

To hedge this risk, we have external resources—

including unused credit facilities from our major

banks—and internal resources, represented by our

cash flow generating capacity.

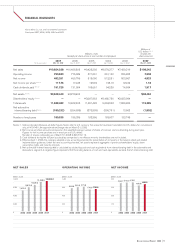

The major components of cash flow are

operating profit, capital expenditures, and changes in

working capital. With our fiscal 2008 operating

capital under pressure, we have to rely on tight

controls of our capital expenditures and limit our

investment to key core projects. We also need to

ensure that each component of working capital is

under constant control and optimization. These

components include accounts receivable, or what our

customers owe us; accounts payable, what we owe

to our suppliers; and every type of inventory, from

new vehicles to used cars to parts and components.

The present worldwide liquidity crisis makes the

monitoring of our cash flow absolutely mandatory,

because it is a clear imperative for our survival.

Alain Dassas

Chief Financial Officer