Motorola 2008 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2008 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

derivative contracts related to the changes in the difference between the spot price and the forward price. These

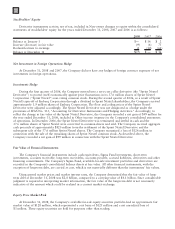

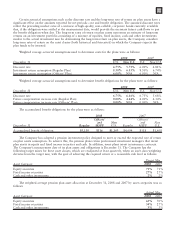

amounts are excluded from the measure of effectiveness. Expense (income) related to cash flow hedges that were

discontinued for the years ended December 31, 2008, 2007 and 2006 are included in the amounts noted above.

During the years ended December 31, 2008, 2007 and 2006, on a pre-tax basis, income (expense) of

$3 million, $(16) million and $(98) million, respectively, was reclassified from equity to earnings in the Company’s

consolidated statements of operations.

At December 31, 2008, the maximum term of derivative instruments that hedge forecasted transactions was

one year. The weighted average duration of the Company’s derivative instruments that hedge forecasted

transactions was seven months.

Interest Rate Risk

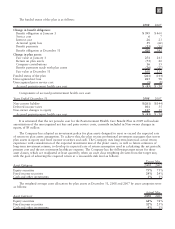

At December 31, 2008, the Company’s short-term debt consisted primarily of $89 million of short-term

variable rate foreign debt. The Company has $4.1 billion of long-term debt, including the current portion of long-

term debt, which is primarily priced at long-term, fixed interest rates.

As part of its liability management program, the Company historically entered into interest rate swaps

(“Hedging Agreements”) to synthetically modify the characteristics of interest rate payments for certain of its

outstanding long-term debt from fixed-rate payments to short-term variable rate payments. During the fourth

quarter of 2008, the Company terminated all of its Hedging Agreements. The termination of the Hedging

Agreements resulted in cash proceeds of approximately $158 million and a gain of approximately $173 million,

which has been deferred and will be recognized as a reduction of interest expense over the remaining term of the

associated debt.

Prior to the termination of the Hedging Agreements in the fourth quarter of 2008, the Hedging Agreements

were designated as part of fair value hedging relationships of the Company’s long-term debt. As such, the changes

in fair value of the Hedging Agreements and corresponding adjustments to the carrying amount of the debt were

recognized in earnings. Interest expense on the debt was adjusted to include payments made or received under such

Hedge Agreements. During 2008 (prior to the Hedging Agreements being terminated) and 2007, the Company

recognized expense of $1 million and $2 million, respectively, representing the ineffective portion of changes in the

fair value of the Hedging Agreements. These amounts are included in Other within Other income (expense) in the

Company’s consolidated statement of operations.

Certain of the terminated Hedging Agreements were originally entered into during the fourth quarter of 2007.

The Company entered into the Hedging Agreements concurrently with issuance of long-term debt to convert the

fixed rate interest cost on the newly issued debt to a floating rate. The Hedging Agreements were originally

designated as fair value hedges of the underlying debt, including the Company’s credit spread. During the first

quarter of 2008, the swaps were no longer considered effective hedges because of the volatility in the price of the

Company’s fixed-rate domestic term debt and the swaps were dedesignated. In the same period, the Company was

able to redesignate the same Hedging Agreements as fair value hedges of the underlying debt, exclusive of the

Company’s credit spread. For the period of time that the Hedging Agreements were deemed ineffective hedges, the

Company recognized a gain of $24 million in the Company’s consolidated statements of operations, representing

the increase in the fair value of the Hedging Agreements.

Additionally, one of the Company’s European subsidiaries has outstanding interest rate agreements (“Interest

Agreements”) relating to a Euro-denominated loan. The interest on the Euro-denominated loan is variable. The

Interest Agreements change the characteristics of interest rate payments from variable to maximum fixed-rate

payments. The Interest Agreements are not accounted for as a part of a hedging relationship and, accordingly, the

changes in the fair value of the Interest Agreements are included in Other income (expense) in the Company’s

consolidated statements of operations. The weighted average fixed rate payments on these Interest Agreements was

5.07%. The fair value of the Interest Agreements at December 31, 2008 and 2007 were $(2) million and

$3 million, respectively.

The Company is exposed to credit loss in the event of nonperformance by the counterparties to its swap

contracts. The Company minimizes its credit risk concentration on these transactions by distributing these

contracts among several leading financial institutions, all of whom presently have investment grade credit ratings,

and having collateral agreements in place. The Company does not anticipate nonperformance.

101