Microsoft 2010 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2010 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

26

loaned securities with the amount determined based upon the underlying security lent and the creditworthiness of the

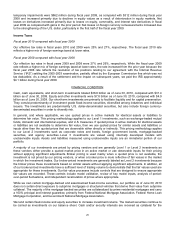

borrower. Cash received is recorded as an asset with a corresponding liability.

Debt

In September 2008, our Board of Directors authorized debt financings of up to $6.0 billion. As of June 30, 2010, we

had $6.0 billion of issued and outstanding debt comprised of $1.0 billion of commercial paper and $5.0 billion of long-

term debt including $1.25 billion of convertible debt.

Short-term Debt

As of June 30, 2010, our $1.0 billion of commercial paper issued and outstanding had a weighted average interest

rate, including issuance costs, of 0.20% and maturities of 22 to 216 days. In November 2009, we replaced our $2.0

billion and $1.0 billion credit facilities with a $2.25 billion 364-day credit facility, which expires on November 5, 2010.

This facility serves as a back-up for our commercial paper program. In June 2010, we reduced the size of our credit

facility from $2.25 billion to $1.0 billion due to the reduction in commercial paper outstanding. As of June 30, 2010,

we were in compliance with the financial covenant in the credit facility agreement, which requires a coverage ratio be

maintained of at least three times earnings before interest, taxes, depreciation, and amortization to interest expense.

No amounts were drawn against the credit facility during any of the periods presented.

Long-term Debt

Notes

As of June 30, 2010, we had issued and outstanding $3.75 billion of debt securities as follows: $2.0 billion aggregate

principal amount of 2.95% notes due 2014, $1.0 billion aggregate principal amount of 4.20% notes due 2019, and

$750 million aggregate principal amount of 5.20% notes due 2039 (collectively “the Notes”). Interest on the Notes is

payable semi-annually on June 1 and December 1 of each year to holders of record on the preceding May 15 and

November 15. The Notes are senior unsecured obligations and rank equally with our other unsecured and

unsubordinated debt outstanding.

Convertible Debt

In June 2010, we issued $1.25 billion of zero coupon convertible unsecured debt due on June 15, 2013 in a private

placement offering. Proceeds from the offering were $1.24 billion, net of fees and expenses which were capitalized.

The majority of the proceeds were used to repay outstanding commercial paper, leaving $1.0 billion of commercial

paper outstanding as of June 30, 2010. Each $1,000 principal amount of notes is convertible into 29.94 shares of

Microsoft common stock at a conversion price of $33.40 per share.

Prior to March 15, 2013, the notes will be convertible, only in certain circumstances, into cash and, if applicable,

cash, shares of Microsoft’s common stock or a combination thereof, at our election. On or after March 15, 2013, the

notes will be convertible at any time. Upon conversion, we will pay cash up to the aggregate principal amount of the

notes and pay or deliver cash, shares of our common stock or a combination of cash and shares of our common

stock, at our election.

Because the convertible debt may be wholly or partially settled in cash, we are required to separately account for the

liability and equity components of the notes in a manner that reflects our nonconvertible debt borrowing rate when

interest costs are recognized in subsequent periods. The net proceeds of $1.24 billion were allocated between debt

for $1.18 billion and stockholders’ equity for $58 million, with the portion in stockholders’ equity representing the fair

value of the option to convert the debt.

In connection with the issuance of the notes, we entered into capped call transactions with certain option

counterparties who are initial purchasers of the notes or their affiliates. The capped call transactions are expected to

reduce potential dilution of earnings per share upon conversion of the notes. Under the capped call transactions, we

purchased from the option counterparties capped call options that in the aggregate relate to the total number of

shares of our common stock underlying the notes, with a strike price equal to the conversion price of the notes and

with a cap price initially equal to $37.16. The purchased capped calls were valued at $40 million and were charged to

stockholders’ equity.