Kia 2004 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2004 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

55

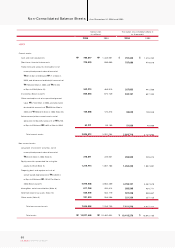

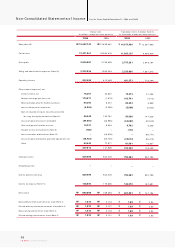

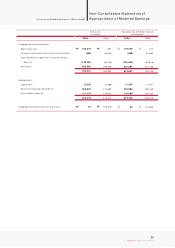

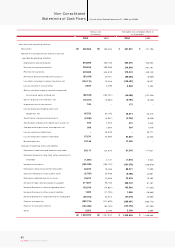

KIA Motors_2004 Annual Report

Accounting principles and auditing standards and their application in practice vary among countries. The accompanying non-

consolidated financial statements are not intended to present the financial position, results of operations and cash flows in

accordance with accounting principles and practices generally accepted in countries and jurisdictions other than the Republic

of Korea. In addition, the procedures and practices utilized in the Republic of Korea to audit such financial statements may differ

from those generally accepted and applied in other countries. Accordingly, this report and the accompanying financial

statements are intended for use by those knowledgeable about Korean accounting procedures and auditing standards and their

application in practice.

Deloitte HanaAnjin LLC

(A Member Firm of Deloitte Touche Tohmatsu)

Seoul, Korea

March 5, 2005

Notice to Readers

This report is effective as of March 5, 2005, the auditors' report date. Certain subsequent events or circum stances may have

occurred betw een the auditors' report date and the time the auditors' report is read. Such events or circumstances could

significantly affect the accompanying financial statements and may result in modifications to the auditors' report.