Frontier Communications 2012 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2012 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106

|

|

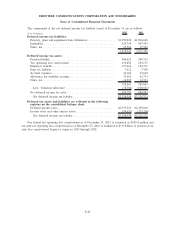

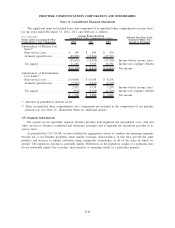

The OPEB plan’s expected benefit payments over the next 10 years are as follows:

($ in thousands)

Year

Gross

Benefits

Medicare Part D

Subsidy Total

2013 $ 14,010 $ 430 $ 13,580

2014 15,591 533 15,058

2015 17,448 644 16,804

2016 19,457 760 18,697

2017 21,347 924 20,423

2018-2022 131,410 7,838 123,572

Total $219,263 $11,129 $208,134

For purposes of measuring year-end benefit obligations, we used, depending on medical plan coverage for

different retiree groups, an 8.0% annual rate of increase in the per-capita cost of covered medical benefits,

gradually decreasing to 5% in the year 2019 and remaining at that level thereafter. The effect of a 1% increase

in the assumed medical cost trend rates for each future year on the aggregate of the service and interest cost

components of the total postretirement benefit cost would be $1.3 million and the effect on the accumulated

postretirement benefit obligation for health benefits would be $19.8 million. The effect of a 1% decrease in the

assumed medical cost trend rates for each future year on the aggregate of the service and interest cost

components of the total postretirement benefit cost would be $(1.0) million and the effect on the accumulated

postretirement benefit obligation for health benefits would be $(16.1) million.

In December 2003, the Medicare Prescription Drug Improvement and Modernization Act of 2003 (the Act)

became law. The Act introduced a prescription drug benefit under Medicare. It includes a federal subsidy to

sponsors of retiree health care benefit plans that provide a benefit that is at least actuarially equivalent to the

Medicare Part D benefit. The amount of the federal subsidy is based on 28% of an individual beneficiary’s

annual eligible prescription drug costs ranging between $250 and $5,000. We have determined that the

Company-sponsored postretirement healthcare plans that provide prescription drug benefits are actuarially

equivalent to the Medicare Prescription Drug benefit. The impact of the federal subsidy has been incorporated

into the calculation.

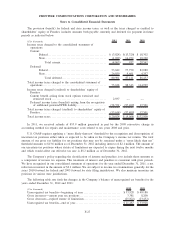

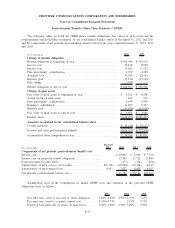

The amounts in accumulated other comprehensive loss that have not yet been recognized as components of

net periodic benefit cost at December 31, 2012 and 2011 are as follows:

($ in thousands) 2012 2011 2012 2011

Pension Plan OPEB

Net actuarial loss ................................. $697,511 $574,998 $105,970 $ 82,841

Prior service cost/(credit) . . ........................ 363 165 (31,706) (41,030)

Total . .......................................... $697,874 $575,163 $ 74,264 $ 41,811

The amounts recognized as a component of accumulated comprehensive loss for the years ended

December 31, 2012 and 2011 are as follows:

($ in thousands) 2012 2011 2012 2011

Pension Plan OPEB

Accumulated other comprehensive loss at beginning

of year ........................................... $575,163 $349,264 $41,811 $13,369

Net actuarial gain (loss) recognized during year ...... (29,890) (15,364) (7,537) (4,424)

Prior service (cost)/credit recognized during year ..... 199 199 10,068 10,198

Net actuarial loss (gain) occurring during year........ 152,402 241,064 30,665 22,668

Prior service cost (credit) occurring during year ...... — — (743) —

Net amount recognized in comprehensive income for

the year .......................................... 122,711 225,899 32,453 28,442

Accumulated other comprehensive loss at end of year. $697,874 $575,163 $74,264 $41,811

F-36

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements