Frontier Communications 2012 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2012 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

|

|

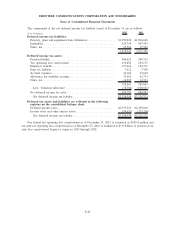

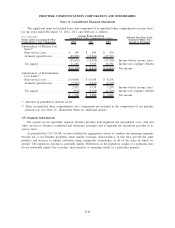

include the following: discount rates, expected long-term rate of return on plan assets, future compensation

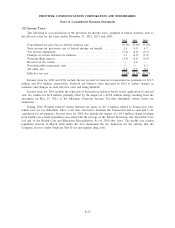

increases, employee turnover, healthcare cost trend rates, expected retirement age, optional form of benefit and

mortality. We review these assumptions for changes annually with our independent actuaries. We consider our

discount rate and expected long-term rate of return on plan assets to be our most critical assumptions.

The discount rate is used to value, on a present value basis, our pension and other postretirement benefit

obligations as of the balance sheet date. The same rate is also used in the interest cost component of the

pension and postretirement benefit cost determination for the following year. The measurement date used in the

selection of our discount rate is the balance sheet date. Our discount rate assumption is determined annually

with assistance from our independent actuaries based on the pattern of expected future benefit payments and the

prevailing rates available on long-term, high quality corporate bonds that approximate the benefit obligation.

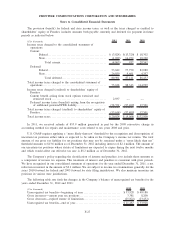

Since the completion of the Transaction on July 1, 2010, we have focused on integrating the operations

and converging the processes of the Acquired Business to effectively operate as one business. During the past

two years, we have worked with Verizon and our third party actuaries to merge the plans, finalize the transfer

of plan assets and ensure we have all the information necessary to make well informed decisions. Based on the

underlying changes in demographics and cash flows, we amended the estimation techniques regarding its

actuarial assumptions, where appropriate, across all of our pension and postretirement plans. The most

significant of such changes was in the estimation technique utilized to develop the discount rate for its pension

and postretirement benefit plans. The revised estimation technique is based upon a settlement model

(Bond:Link) of such liabilities as of December 31, 2012 that permits us to more closely match cash flows to the

expected payments to participants than would be possible with the previously used yield curve model. We

believe such a change results in an estimate of the discount rate that more accurately reflects the settlement

value for plan obligations than the different yield curve methodologies used in prior years, as it provides the

ability to review the quality and diversification of the portfolio to select the bond issues that would settle the

obligation in an optimal manner. This rate can change from year-to-year based on market conditions that affect

corporate bond yields.

In determining the discount rate as of December 31, 2011 and 2010, we considered, among other things,

the yields on the Citigroup Above Median Pension Curve, the Towers Watson Index, the general movement of

interest rates and the changes in those rates from one period to the next.

As a result of the change described above, Frontier is utilizing a discount rate of 4.00% as of December

31, 2012 for its qualified pension plan, compared to rates of 4.50% and 5.25% in 2011 and 2010, respectively.

Had the previous estimation technique been used, the discount rate would have been 3.75% in comparison to

the 4.00% discount rate, and the impact to the projected benefit obligation at December 31, 2012 would have

been immaterial. The discount rate for postretirement plans as of December 31, 2012 was a range of 4.00% to

4.20% compared to a range of 4.50% to 4.75% in 2011 and 5.25% in 2010.

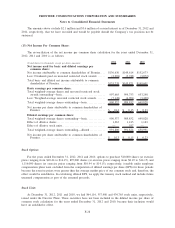

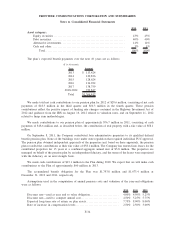

The expected long-term rate of return on plan assets is applied in the determination of periodic pension

and postretirement benefit cost as a reduction in the computation of the expense. In developing the expected

long-term rate of return assumption, we considered published surveys of expected market returns, 10 and 20

year actual returns of various major indices, and our own historical 5-year, 10-year and 20-year investment

returns. The expected long-term rate of return on plan assets is based on an asset allocation assumption of 35%

to 55% in fixed income securities, 35% to 55% in equity securities and 5% to 15% in alternative investments.

We review our asset allocation at least annually and make changes when considered appropriate. Our pension

asset investment allocation decisions are made by the Retirement Investment & Administration Committee

(RIAC), a committee comprised of members of management, pursuant to a delegation of authority by the

Retirement Plan Committee of the Board of Directors. The RIAC is responsible for reporting its actions to the

Retirement Plan Committee. Asset allocation decisions take into account expected market return assumptions of

various asset classes as well as expected pension benefit payment streams. When analyzing anticipated benefit

payments, management considers both the absolute amount of the payments as well as the timing of such

payments. In 2012, 2011 and 2010, our expected long-term rate of return on plan assets was 7.75%, 8.00% and

8.00%, respectively. For 2013, we will assume a rate of return of 8.00%. Our pension plan assets are valued at

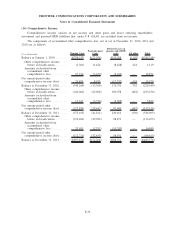

F-32

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements