Frontier Communications 2012 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2012 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

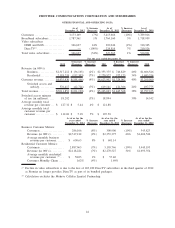

partially offset by the impact of a $10.8 million charge resulting from the enactment on May 25, 2011 of the

Michigan Corporate Income Tax that eliminated certain future tax deductions.

The higher rate in 2010 was primarily related to the write-off of certain deferred tax assets in 2010 of

$11.3 million related to Transaction costs which were not tax deductible. Prior to the closing of the

Transaction, these costs were deemed to be tax deductible as the Transaction had not yet been successfully

completed. These costs were incurred to facilitate the Transaction and once the Transaction closed, these costs

had to be capitalized for tax purposes.

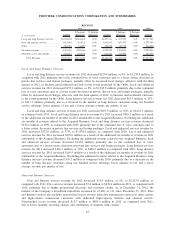

Contingencies

See Note 19 of the Notes to Consolidated Financial Statements included in Part IV of this report for a

discussion of commitments and contingencies. Our contingencies include the potential obligation associated

with our previous electric utility activities in the state of Vermont, along with ongoing regulatory issues and

legal cases in the normal course of our business, including billing disputes.

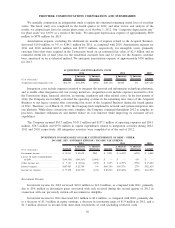

Purchase Price Allocation—The Transaction

The allocation of the approximate $5.4 billion in total consideration to the “fair market value” of the assets

and liabilities of the Acquired Business is a critical estimate. The estimates of the fair values assigned to plant,

customer base and goodwill, are more fully described in Notes 3 and 6 of the Notes to Consolidated Financial

Statements. Additionally, the estimated expected life of a customer (used to amortize the customer base) is a

critical estimate.

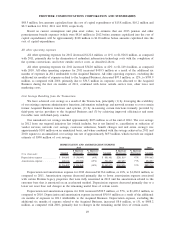

New Accounting Pronouncements

There were no new accounting standards issued and adopted by the Company in 2012, or that have been

issued but are not required to be adopted until future periods, with any material financial statement impact.

Fair Value Measurements

In May 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update

(ASU) No. 2011-04 (ASU 2011-04), “Fair Value Measurements: Amendments to Achieve Common Fair Value

Measurement and Disclosure Requirements in U.S. GAAP and IFRSs” (Accounting Standards Codification

(ASC) Topic 820). ASU 2011-04 changes the wording used to describe many of the requirements in U.S.

GAAP for measuring fair value and for disclosing information about fair value measurements to ensure

consistency between U.S. GAAP and IFRS. ASU 2011-04 also expands the disclosures for fair value

measurements that are estimated using significant unobservable (Level 3) inputs. This new guidance was to be

applied prospectively, and was effective for interim and annual periods beginning after December 15, 2011.

The Company adopted ASU 2011-04 in the first quarter of 2012 with no impact on our financial position,

results of operations or cash flows.

Presentation of Comprehensive Income

In June 2011, the FASB issued ASU No. 2011-05 (ASU 2011-05), “Comprehensive Income: Presentation

of Comprehensive Income,” (ASC Topic 220). ASU 2011-05 eliminates the option to report other

comprehensive income and its components in the statement of changes in equity. ASU 2011-05 requires

that all non-owner changes in stockholders’ equity be presented in either a single continuous statement of

comprehensive income or in two separate but consecutive statements. This new guidance was to be applied

retrospectively, and was effective for interim and annual periods beginning after December 15, 2011. The

Company adopted ASU 2011-05 in the first quarter of 2012 with no impact on our financial position, results of

operations or cash flows.

In February 2013, the FASB issued ASU No. 2013-02 (ASU 2013-02), “Comprehensive Income:

Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income,” (ASC Topic 220).

ASU 2013-02 requires disclosing the effect of reclassifications out of accumulated other comprehensive income

on the respective line items in net income in circumstances when U.S. GAAP requires the item being

reclassified in its entirety to net income. This new guidance is to be applied prospectively. The Company

41

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES