Energizer 2013 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2013 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

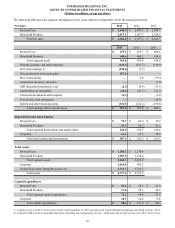

ENERGIZER HOLDINGS, INC.

(Dollars in millions, except per share data)

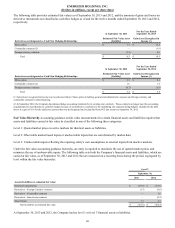

For the twelve months ended September 30, 2013, total dividends declared to shareholders were $108.1 of which $105.6 were

paid.

Subsequent to the end of fiscal 2013, on November 4, 2013, the Company's Board of Directors declared a dividend for the first

quarter of fiscal 2014 of $0.50 per share of Common Stock, which will be paid on December 17, 2013 and is expected to be

approximately $31.

On June 4, 2013, the Company retired approximately 43 million shares of its treasury stock. These shares are now authorized

but unissued. In accordance with ASC section 505, the treasury stock retirement resulted in a reduction of the following on the

Company's Consolidated Balance Sheet: treasury stock by $2,146.5, common stock by $0.4 and retained earnings by $2,146.1.

There was no effect on the Company's total shareholders' equity as a result of the retirement.

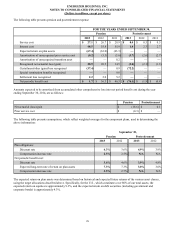

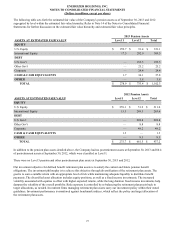

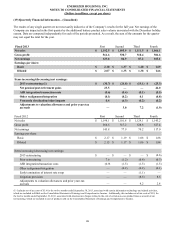

(14) Financial Instruments and Risk Management

The market risk inherent in the Company’s financial instruments and positions represents the potential loss arising from adverse

changes in currency rates, commodity prices, interest rates and the Company’s stock price. Company policy allows derivatives

to be used only for identifiable exposures and, therefore, the Company does not enter into hedges for trading purposes where

the sole objective is to generate profits.

Concentration of Credit Risk The counterparties to derivative contracts consist of a number of major financial institutions and

are generally institutions with which the Company maintains lines of credit. The Company does not enter into derivative

contracts through brokers nor does it trade derivative contracts on any other exchange or over-the-counter markets. Risk of

currency positions and mark-to-market valuation of positions are strictly monitored at all times.

The Company continually monitors positions with, and credit ratings of, counterparties both internally and by using outside

rating agencies. The Company has implemented policies that limit the amount of agreements it enters into with any one party.

While nonperformance by these counterparties exposes the Company to potential credit losses, such losses are not anticipated.

The Company sells to a large number of customers primarily in the retail trade, including those in mass merchandising,

drugstore, supermarket and other channels of distribution throughout the world. Wal-Mart Stores, Inc. and its subsidiaries

accounted for 20.0%, 20.3% and 19.5% of total net sales in fiscal 2013, 2012 and 2011, respectively, primarily in North

America. The Company performs ongoing evaluations of its customers' financial condition and creditworthiness, but does not

generally require collateral. The Company’s largest customer had obligations to the Company with a carrying value of $80.2 at

September 30, 2013. While the competitiveness of the retail industry presents an inherent uncertainty, the Company does not

believe a significant risk of loss from a concentration of credit risk exists with respect to accounts receivable.

In the ordinary course of business, the Company enters into contractual arrangements (derivatives) to reduce its exposure to

foreign currency, interest rate and commodity price risks. The section below outlines the types of derivatives that existed at

September 30, 2013 and 2012 as well as the Company’s objectives and strategies for holding these derivative instruments.

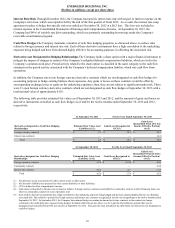

Commodity Price Risk The Company uses raw materials that are subject to price volatility. At times, the Company has used,

and may in the future use, hedging instruments to reduce exposure to variability in cash flows associated with future purchases

of certain materials and commodities. At September 20, 2013, there were no open derivative or hedging instruments for future

purchases of raw materials or commodities.

Foreign Currency Risk A significant portion of the Company’s product cost is more closely tied to the U.S. dollar than to the

local currencies in which the product is sold. As such, a weakening of currencies relative to the U.S. dollar, results in margin

declines unless mitigated through pricing actions, which are not always available due to the economic or competitive

environment. Conversely, a strengthening in currencies relative to the U.S. dollar can improve margins. As a result, the

Company has entered into a series of forward currency contracts to hedge the cash flow uncertainty of forecasted inventory

purchases due to short term currency fluctuations. The Company’s primary foreign affiliates, which are exposed to U.S. dollar

purchases, have the Euro, the Japanese yen, the British pound, the Canadian dollar and the Australian dollar as their local

currencies. At September 30, 2013 and 2012, the Company had an unrealized pre-tax gain on these forward currency contracts

accounted for as cash flow hedges of $1.5 and an unrealized pre-tax loss of $5.9, respectively, included in Accumulated other

comprehensive loss on the Consolidated Balance Sheets. Assuming foreign exchange rates versus the U.S. dollar remain at

September 30, 2013 levels, over the next twelve months, approximately $1.9 of the pre-tax gain included in Accumulated other

comprehensive loss will be included in earnings. Contract maturities for these hedges extend into fiscal year 2014. There were

80 open contracts at September 30, 2013 with a total notional value of approximately $339.

80