Dish Network 2003 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2003 Dish Network annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

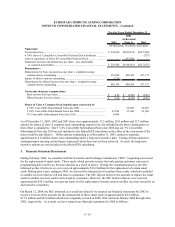

ECHOSTAR COMMUNICATIONS CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – Continued

F–13

Long-lived Assets

We account for long-lived assets in accordance with the provision of Statement of Financial Accounting Standards

No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets” (“FAS 144”). We review our long-

lived assets and identifiable intangible assets for impairment whenever events or changes in circumstances indicate

that the carrying amount of an asset may not be recoverable. For assets which are held and used in operations, the

asset would be impaired if the book value of the asset (or asset group) exceeded its undiscounted future net cash

flows. Once an impairment is determined, the actual impairment is reported as the difference between the book

value and the fair market value as estimated using discounted cash flows. Assets which are to be disposed of are

reported at the lower of the carrying amount or fair market value less costs to sell. We consider relevant cash flow,

estimated future operating results, trends and other available information in assessing whether the carrying value of

assets are recoverable.

Goodwill and Intangible Assets

The excess of investment in consolidated subsidiaries over net tangible and intangible asset value at acquisition is

recorded as goodwill. Our intangible assets consist primarily of FCC licenses. On January 1, 2002, we adopted

Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (“FAS 142”), which

requires goodwill and intangible assets with indefinite useful lives not be amortized but to be tested for impairment

annually or whenever indicators of impairments arise. Intangible assets that have finite lives continue to be

amortized over their estimated useful lives. The amortization and non-amortization provisions of FAS 142 were

applied to all goodwill and intangible assets acquired after September 30, 2001. As of January 1, 2002, our FCC

licenses have indefinite useful lives and are no longer amortized because:

• FCC spectrum is a non-depleting asset;

• Existing DBS licenses are integral to our business and will contribute to cash flows indefinitely;

• Replacement satellite applications are generally authorized by the FCC subject to certain conditions,

without substantial cost under a stable regulatory, legislative and legal environment;

• Maintenance expenditures in order to obtain future cash flows are not significant;

• DBS licenses are not technologically dependent; and

• We intend to use these assets for the foreseeable future.

Had we not amortized our FCC licenses during the year ended December 31, 2001, our net loss would have

decreased by approximately $18.8 million, or $0.04 per common share.

At January 1, 2002, we did not have any goodwill. In accordance with FAS 142, we tested our indefinite-lived

intangible assets (consisting of FCC licenses) and determined that there was no impairment required because the fair

market value of such assets exceeded the carrying value.

In accordance with the guidance of EITF Issue No. 02-7, “Unit of Accounting for Testing Impairment of Indefinite-

Lived Intangible Asset,” ("EITF 02-7”) we combine all our indefinite life FCC licenses into a single unit of

accounting. The analysis encompasses future cash flows from satellites transmitting from such licensed orbital

locations, including revenue attributable to programming offerings from such satellites, the direct operating and

subscriber acquisition costs related to such programming, and future capital costs for replacement satellites.

Projected revenue and cost amounts included current and projected subscribers. In conducting our annual

impairment test in 2003, we determined that the estimated fair market value of the FCC licenses, calculated using

the discounted cash flow analysis, exceeded their carrying amount.