Classmates.com 2006 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2006 Classmates.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

|

|

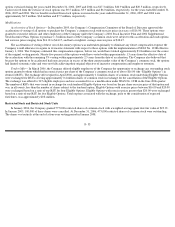

purposes and the interest rates on borrowings were based on current market rates. The line of credit contained covenants pertaining to the

maintenance of a minimum quick ratio, minimum cash balances with the lender and minimum profitability levels. The line of credit provided

additional working capital to support the Company’s growth and overall business strategy.

In November 2004, the Company borrowed $10.3 million from the line of credit and repaid the amount on the same business day. The line

of credit was canceled in December 2004 in connection with the signing of the term loan agreement under which the Company borrowed

$100 million.

Term Loan and Interest Rate Cap

In December 2004, the Company borrowed $100 million through a term loan facility dated December 3, 2004. A small portion of the

proceeds of the term loan facility were used to purchase shares tendered pursuant to the Company’s tender offer and to pay related fees and

expenses. The funds were available for general corporate purposes, stock repurchases and acquisitions, subject to certain limitations.

The term loan was to mature in four years and amortized in an annual amount of $23.3 million in years one, two and three and $30 million

in year four, payable in quarterly installments. Any voluntarily prepayments made by the Company reduced, on a pro-rata basis, the remaining

outstanding amortization payments. The Company had the option to maintain the term loan as either base rate loans or Eurodollar loans, but at

no time could there be outstanding more than four Eurodollar loans. Interest on the loans outstanding under the term loan facility was payable, at

the Company’s option, at (a) a base rate equal to the higher of (i) the prime rate plus a margin of 2% and (ii) 0.50% in excess of the overnight

federal funds rate plus a margin of 2% or (b) at a eurodollar rate generally equal to LIBOR with a maturity comparable to a selected interest

period, plus a margin of 3%.

The Company was able to make optional prepayments of the term loan, in whole or in part (subject to a minimum prepayment amount),

without premium or penalty, and subject to the reimbursement of lenders’ customary breakage costs in the case of a prepayment of Eurodollar

borrowings. Subject to certain limitations, the Company was required to make prepayments of a portion of the term loan from excess cash flow

(commencing in the first quarter of 2006), proceeds of asset sales, insurance recovery and condemnation events and the issuance of equity and

debt. During the year ended December 31, 2005, the Company made voluntary prepayments of $28.8 million on the term loan which reduced

future principal repayments on a pro rata basis.

The facility was collateralized by substantially all of the Company’s assets and was unconditionally guaranteed by each of the Company’s

domestic subsidiaries.

The credit agreement contained certain financial and other covenants that placed restrictions on additional indebtedness by the Company,

liens against the Company’s assets, payment of dividends, consolidation, merger, purchase or sale of assets, capital expenditures, investments

and acquisitions. At December 31, 2005, the Company was in compliance with all covenants.

The credit agreement also included certain customary events of default such as payment defaults, cross defaults to other indebtedness,

bankruptcy and insolvency, and a change in control, the occurrence of which would cause all amounts under the agreement to become

immediately due and payable. At December 31, 2005, no events of default had occurred.

On January 31, 2005, the Company purchased an interest-rate cap to reduce the variability in the amount of expected future cash interest

payments that were attributable to LIBOR-based market interest rates. The interest-rate cap was designated and qualified as a cash flow hedge.

The Company paid a $0.2 million premium to enter into the cap, which provided protection through January 31, 2007 on $25 million of the

Company’

s outstanding term loan balance. The cap protected the Company from an increase in three month LIBOR over 3.5% on $25 million of

borrowings over a two-year term. Changes in the fair

F- 28