CarMax 2002 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2002 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

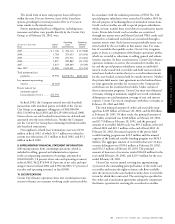

15. RECENT ACCOUNTING PRONOUNCEMENTS

In July 2000, the Financial Accounting Standards Board issued

Emerging Issues Task Force Issue No. 00-14, “Accounting for

Certain Sales Incentives,” which is effective for fiscal quarters

beginning after December 15, 2001. EITF No. 00-14 provides

that sales incentives, such as mail-in rebates, offered to customers

should be classified as a reduction of revenue. The Company

offers certain mail-in rebates that are currently recorded in cost of

sales, buying and warehousing. However, in the first quarter of fis-

cal 2003, the Company expects to reclassify these rebate expenses

from cost of sales, buying and warehousing to net sales and oper-

ating revenues to be in compliance with EITF No. 00-14. On a

pro forma basis, this reclassification would have increased the fiscal

2002 Circuit City Group gross profit margin by 18 basis points

and the expense ratio by 17 basis points. For fiscal 2001, the

reclassification would have increased the gross profit margin by

29 basis points and the expense ratio by 27 basis points. The

Company does not expect the adoption of EITF No. 00-14 to

have a material impact on the Group’s financial position, results

of operations or cash flows.

In August 2001, the FASB issued SFAS No. 143, “Account-

ing For Asset Retirement Obligations.” This statement addresses

financial accounting and reporting for obligations associated

with the retirement of tangible long-lived assets and the associ-

ated asset retirement costs. It applies to legal obligations asso-

ciated with the retirement of long-lived assets that result from

the acquisition, construction, development and/or the normal

operation of a long-lived asset, except for certain obligations of

lessees. This standard requires entities to record the fair value of

a liability for an asset retirement obligation in the period

incurred. SFAS No. 143 is effective for fiscal years beginning

after June 15, 2002. The Company has not yet determined the

impact, if any, of adopting this standard.

In August 2001, the FASB issued SFAS No. 144, “Account-

ing for the Impairment or Disposal of Long-Lived Assets,”

which supersedes both SFAS No. 121, “Accounting for the

Impairment of Long-Lived Assets and for Long-Lived Assets to

Be Disposed Of,” and the accounting and reporting provisions

of APB Opinion No. 30, “Reporting the Results of Operations-

Reporting the Effects of Disposal of a Segment of a Business,

and Extraordinary, Unusual and Infrequently Occurring Events

and Transactions,” related to the disposal of a segment of a

business (as previously defined in that Opinion). SFAS No. 144

retains the fundamental provisions in SFAS No. 121 for recog-

nizing and measuring impairment losses on long-lived assets

held for use and long-lived assets to be disposed of by sale,

while also resolving significant implementation issues associated

with SFAS No. 121. The Company is required to adopt SFAS

No. 144 no later than the fiscal year beginning after December

15, 2001, and plans to adopt the provisions in the first quarter

of fiscal 2003. The Company does not expect the adoption of

SFAS No. 144 to have a material impact on the Group’s finan-

cial position, results of operations or cash flows.

CIRCUIT CITY STORES, INC. ANNUAL REPORT 2002 76