Capital One 2000 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2000 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70

|

|

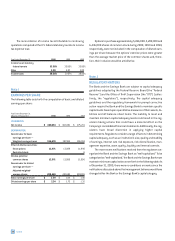

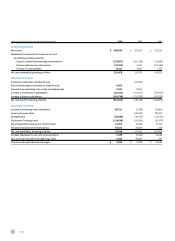

In 1999, the Company entered into two three-year agree-

ments for the lease of four facilities located in Tampa, Florida and

Federal Way, Washington. Monthly rent commences upon com-

pletion of each of the buildings. At December 31, 2000, the

construction of two of the facilities has been completed and rent

payments have commenced. The Company has a one year renewal

option under the terms of the leases. The Company guarantees a

residual value to the lessor of up to approximately 85% of the cost

of the buildings in the lease agreement.

In 1998, the Company entered into a five-year lease of five

facilities in Tampa, Florida and Richmond, Virginia. The Company has

two one-year renewal options under the terms of the lease. If, at the

end of the lease term, the Company does not purchase all of the

properties, the Company guarantees a residual value to the lessor

of up to approximately 84% of the costs of the buildings.

In connection with the transfer of substantially all of Signet

Bank’s credit card business to the Bank in November 1994, the

Company and the Bank agreed to indemnify Signet Bank (which

was acquired by First Union on November 30, 1997) for certain lia-

bilities incurred in litigation arising from that business, which may

include liabilities, if any, incurred in the purported class action case

described below.

During 1995, the Company and the Bank became involved in

a purported class action suit relating to certain collection practices

engaged in by Signet Bank and, subsequently, by the Bank. The

complaint in this case alleges that Signet Bank and/or the Bank vio-

lated a variety of California state statutes and constitutional and

common law duties by filing collection lawsuits, obtaining judge-

ments and pursuing garnishment proceedings in the Virginia state

courts against defaulted credit card customers who were not resi-

dents of Virginia. This case was filed in the Superior Court of

California in the County of Alameda, Southern Division, on behalf of

a class of California residents. The complaint in this case seeks

unspecified statutory damages, compensatory damages, punitive

damages, restitution, attorneys’ fees and costs, a permanent

injunction and other equitable relief.

In early 1997, the California court entered judgement in favor

of the Bank on all of the plaintiffs’ claims. The plaintiffs appealed

the ruling to the California Court of Appeals First Appellate District

Division 4. In early 1999, the Court of Appeals affirmed the trial

court’s ruling in favor of the Bank on six counts, but reversed the

trial court’s ruling on two counts of the plaintiffs’ complaint. The Cal-

ifornia Supreme Court rejected the Bank’s Petition for Review of the

remaining two counts and remitted them to the trial court for fur-

ther proceedings. In August 1999, the trial court denied without

prejudice plaintiffs’ motion to certify a class on the one remaining

common law claim. In November 1999, the United States Supreme

Court denied the Bank’s writ of certiorari on the remaining two

counts, declining to exercise its discretionary power to review these

issues.

Subsequently, the Bank moved for summary judgment on the

two remaining counts and for a ruling that a class cannot be certi-

fied in this case. The motion for summary judgment was granted

in favor of the Bank on both counts, but the plaintiffs were granted

leave to amend their complaint. Plaintiffs have filed an Amended

Complaint, to which the Bank filed demurrers and motions to strike;

those responses are pending before the court.

Because no specific measure of damages is demanded in the

complaint of the California case and the trial court entered judgment

in favor of the Bank early in the case, an informed assessment of

the ultimate outcome of this case cannot be made at this time. Man-

agement believes, however, that there are meritorious defenses to

this lawsuit and intends to defend it vigorously.

The Company is commonly subject to various other pending

and threatened legal actions arising from the conduct of its normal

business activities. In the opinion of management, the ultimate

aggregate liability, if any, arising out of any pending or threatened

action will not have a material adverse effect on the consolidated

financial condition of the Company. At the present time, however,

management is not in a position to determine whether the resolu-

tion of pending or threatened litigation will have a material effect on

the Company’s results of operations in any future reporting period.

Note L

RELATED PARTY TRANSACTIONS

In the ordinary course of business, executive officers and directors

of the Company may have consumer loans issued by the Company.

Pursuant to the Company’s policy, such loans are issued on the

same terms as those prevailing at the time for comparable loans to

unrelated persons and do not involve more than the normal risk of

collectibility.

60 notes