Capital One 2000 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2000 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

|

|

52 notes

Note E

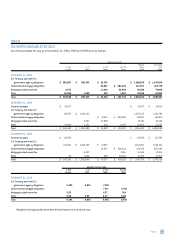

BORROWINGS

Borrowings as of December 31, 2000 and 1999 were as follows:

2000 1999

Weighted Weighted

Average Average

Outstanding Rate Outstanding Rate

INTEREST-BEARING

DEPOSITS $ 8,379,025 6.67% $ 3,783,809 5.34%

OTHER BORROWINGS

Secured borrowings $ 1,773,450 6.76% $ 1,344,790 6.65%

Junior subordinated

capital income

securities 98,436 8.31 98,178 7.76

Federal funds purchased

and resale agreements 1,010,693 6.58 1,240,000 5.84

Other short-term

borrowings 43,359 6.17 97,498 3.97

Total $ 2,925,938 $ 2,780,466

SENIOR NOTES

Bank — fixed rate $ 3,154,555 6.98% $ 3,409,652 6.71%

Bank — variable rate 347,000 7.41 221,999 6.74

Corporation 549,042 7.20 548,897 7.20

Total $ 4,050,597 $ 4,180,548

Interest-bearing Deposits

As of December 31, 2000, the aggregate amount of interest-bearing

deposits with accounts equal to or exceeding $100 was $3,697,888.

Secured Borrowings

Capital One Auto Finance Corporation (formerly Summit Acceptance

Corporation), a subsidiary of the Company, currently maintains

three agreements to transfer pools of consumer loans. The agree-

ments were entered into in December 2000, May 2000 and May

1999, relating to the transfer of pools of consumer loans totaling

$425,000, $325,000 and $350,000, respectively. Proceeds from

the transfers were recorded as secured borrowings. Principal pay-

ments on the borrowings are based on principal collections net of

losses on the transferred consumer loans. The borrowings accrue

interest based on commercial paper rates and mature between

June 2006 and October 2007, or earlier depending upon the repay-

ment of the underlying consumer loans. At December 31, 2000,

and 1999, $870,185 and $290,065, respectively, of the secured

borrowings were outstanding.

Note C

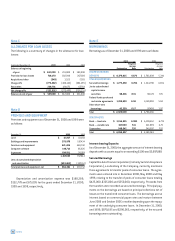

ALLOWANCE FOR LOAN LOSSES

The following is a summary of changes in the allowance for loan

losses:

Year Ended December 31 2000 1999 1998

Balance at beginning

of year $ 342,000 $ 231,000 $ 183,000

Provision for loan losses 718,170 382,948 267,028

Acquisitions/other (549) 3,522 7,503

Charge-offs (772,402) (400,143) (294,295)

Recoveries 239,781 124, 673 67,764

Net charge-offs (532,621) (275,470) (226,531)

Balance at end of year $527,000$ 342,000 $ 231,000

Note D

PREMISES AND EQUIPMENT

Premises and equipment as of December 31, 2000 and 1999 were

as follows:

December 31 2000 1999

Land $ 10,917 $10,168

Buildings and improvements 279,979 197,434

Furniture and equipment 621,404 448,742

Computer software 140,712 86,626

In process 104,911 54,874

1,157,923 797,844

Less: Accumulated depreciation

and amortization (493,462) (327,112)

Total premises and equipment, net $ 664,461 $470,732

Depreciation and amortization expense was $180,289,

$122,778 and $75,005 for the years ended December 31, 2000,

1999 and 1998, respectively.