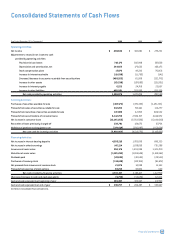

Capital One 2000 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2000 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

38 md&a

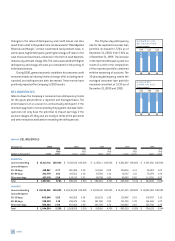

table 12: INTEREST RATE SENSITIVITY

Within >180 Days– >1 Year– Over

As of December 31, 2000 Subject to Repricing (Dollars in Millions) 180 Days 1 Year 5 Years 5 Years

EARNING ASSETS:

Federal funds sold and resale agreements $61

Interest-bearing deposits at other banks 102

Securities available for sale 156 $ 147 $ 895 $ 498

Consumer loans 6,131 6 8,976

Total earning assets 6,450 153 9,871 498

INTEREST-BEARING LIABILITIES:

Interest-bearing deposits 2,647 1,447 3,981 304

Other borrowings 2,826 100

Senior notes 522 143 2,745 641

Total interest-bearing liabilities 5,995 1,690 6,726 945

Non-rate related assets (1,616)

Interest sensitivity gap 455 (1,537) 3,145 (2,063)

Impact of swaps 3,854 (153) (3,592) (109)

Impact of consumer loan securitizations (4,476) (677) 5,853 (700)

Interest sensitivity gap adjusted for impact

of securitizations and swaps $ (167) $ (2,367) $ 5,406 $ (2,872)

Adjusted gap as a percentage of managed assets –0.50% –7.11% 16.24% –8.63%

Adjusted cumulative gap $ (167) $ (2,534) $ 2,872 $ —

Adjusted cumulative gap as a percentage

of managed assets – 0.50% –7.61% 8.63% 0.00%

BUSINESS OUTLOOK

Earnings, Goals and Strategies

This business outlook section summarizes Capital One's expectations

for earnings for the year ending December 31, 2001, and our primary

goals and strategies for continued growth. The statements contained

in this section are based on management’s current expectations.

Certain statements are forward looking and, therefore, actual results

could differ materially. Factors that could materially influence results

are set forth throughout this section and in Capital One's Annual

Report on Form 10-K for the year ended December 31, 2000 (Part I,

Item 1, Risk Factors).

We have set targets, dependent on the factors set forth below, to

achieve a 20% return on equity in 2001 and to increase Capital One's

2001 earnings per share by approximately 30% over earnings per

share for 2000. As discussed elsewhere in this report and below,

Capital One's actual earnings are a function of our revenues (net inter-

est income and non-interest income on our earning assets),

consumer usage and payment patterns, credit quality of our earning

assets (which affects fees and charge-offs), marketing expenses and

operating expenses.

Product and Market Opportunities

Our strategy for future growth has been, and is expected to con-

tinue to be, to apply our proprietary IBS to our lending and

non-lending businesses. We will seek to identify new product oppor-

tunities and to make informed investment decisions regarding new

and existing products. Our lending and other financial and non-

financial products are subject to competitive pressures, which

management anticipates will increase as these markets mature.

Lending

Lending includes credit card and other consumer lending products,

including automobile financing and unsecured installment lending.

Credit card opportunities include, and are expected to continue to

include, a wide variety of highly customized products with interest

rates, credit lines and other features specifically tailored for numer-

ous consumer segments. We expect continued growth across a

broad spectrum of new and existing customized products, which are

distinguished by a range of credit lines, pricing structures and other

characteristics. For example, our low introductory and non-introduc-

tory rate products, which are marketed to consumers with the best