Capital One 2000 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2000 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

md&a 37

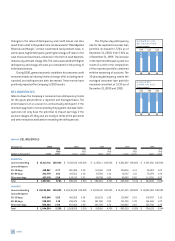

DIVIDEND POLICY

Although the Company expects to reinvest a substantial portion of

its earnings in its business, the Company intends to continue to pay

regular quarterly cash dividends on the Common Stock. The decla-

ration and payment of dividends, as well as the amount thereof, is

subject to the discretion of the Board of Directors of the Company

and will depend upon the Company's results of operations, finan-

cial condition, cash requirements, future prospects and other

factors deemed relevant by the Board of Directors. Accordingly,

there can be no assurance that the Corporation will declare and pay

any dividends. As a holding company, the ability of the Company to

pay dividends is dependent upon the receipt of dividends or other

payments from its subsidiaries. Applicable banking regulations and

provisions that may be contained in borrowing agreements of the

Company or its subsidiaries may restrict the ability of the Com-

pany's subsidiaries to pay dividends to the Corporation or the ability

of the Corporation to pay dividends to its stockholders.

OFF-BALANCE SHEET RISK

The Company is subject to off-balance sheet risk in the normal course

of business including commitments to extend credit, reduce the inter-

est rate sensitivity of its securitization transactions and its

off-balance sheet financial instruments. The Company enters into

interest rate swap agreements in the management of its interest rate

exposure. The Company also enters into forward foreign currency

exchange contracts and currency swaps to reduce its sensitivity to

changing foreign currency exchange rates. These off-balance sheet

financial instruments involve elements of credit, interest rate or for-

eign currency exchange rate risk in excess of the amount recognized

on the balance sheet. These instruments also present the Company

with certain credit, market, legal and operational risks. The Company

has established credit policies for off-balance sheet instruments as

it has for on-balance sheet instruments.

Additional information regarding off-balance sheet financial

instruments can be found in Note N to the Consolidated Financial

Statements.

INTEREST RATE SENSITIVITY

Interest rate sensitivity refers to the change in earnings that may

result from changes in the level of interest rates. To the extent that

managed interest income and expense do not respond equally to

changes in interest rates, or that all rates do not change uniformly,

earnings could be affected. The Company's managed net interest

income is affected by changes in short-term interest rates, prima-

rily the London InterBank Offering Rate, as a result of its issuance of

interest-bearing deposits, variable rate loans and variable rate secu-

ritizations. The Company manages and mitigates its interest rate

sensitivity through several techniques which include, but are not

limited to, changing the maturity, repricing and distribution of assets

and liabilities and entering into interest rate swaps.

The Company measures exposure to its interest rate risk

through the use of a simulation model. The model generates a dis-

tribution of possible twelve-month managed net interest income

outcomes based on (i) a set of plausible interest rate scenarios, as

determined by management based upon historical trends and mar-

ket expectations, (ii) all existing financial instruments, including

swaps, and (iii) an estimate of ongoing business activity over the

coming twelve months. The Company's asset/liability management

policy requires that based on this distribution there be at least a

95% probability that managed net interest income achieved over

the coming twelve months will be no more than 2.5% below the

mean managed net interest income of the distribution. As of

December 31, 2000, the Company was in compliance with the pol-

icy; more than 99% of the outcomes generated by the model

produced a managed net interest income of no more than 1% below

the mean outcome. The interest rate scenarios evaluated as of

December 31, 2000 included scenarios in which short-term interest

rates rose in excess of 400 basis points or fell by as much as 250

basis points over twelve months.

The analysis does not consider the effects of the changed level

of overall economic activity associated with various interest rate

scenarios. Further, in the event of a rate change of large magnitude,

management would likely take actions to further mitigate its expo-

sure to any adverse impact. For example, management may reprice

interest rates on outstanding credit card loans subject to the right

of the consumers in certain states to reject such repricing by giving

timely written notice to the Company and thereby relinquishing

charging privileges. However, competitive factors as well as certain

legal constraints may limit the repricing of credit card loans.

Interest rate sensitivity at a point in time can also be analyzed

by measuring the mismatch in balances of earning assets and inter-

est-bearing liabilities that are subject to repricing in future periods.

Table 12 reflects the interest rate repricing schedule for earn-

ing assets and interest-bearing liabilities as of December 31, 2000.