Avon 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

During 2003, we entered into treasury lock agreements that we designated as cash flow hedges and used to hedge the exposure to the

possible rise in interest rates prior to the issuance of the 4.625% Notes. The loss of $2.6 was recorded in AOCI and is being amortized to

interest expense over ten years.

AOCI included remaining unamortized losses of $22.5 ($14.6 net of taxes) at December 31, 2010, and $28.8 ($18.8 net of taxes) at

December 31, 2009, resulting from treasury lock agreements.

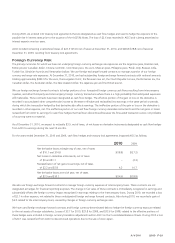

Foreign Currency Risk

The primary currencies for which we have net underlying foreign currency exchange rate exposures are the Argentine peso, Brazilian real,

British pound, Canadian dollar, Chinese renminbi, Colombian peso, the euro, Mexican peso, Philippine peso, Polish zloty, Russian ruble,

Turkish lira, Ukrainian hryvnia and Venezuelan bolívar. We use foreign exchange forward contracts to manage a portion of our foreign

currency exchange rate exposures. At December 31, 2010, we had outstanding foreign exchange forward contracts with notional amounts

totaling approximately $493.9 for the euro, the Hungarian forint, the Peruvian new sol, the Czech Republic koruna, the Romanian leu, the

Canadian dollar, the Australian dollar, the New Zealand dollar, the Japanese yen and the British pound.

We use foreign exchange forward contracts to hedge portions of our forecasted foreign currency cash flows resulting from intercompany

royalties, and other third-party and intercompany foreign currency transactions where there is a high probability that anticipated exposures

will materialize. These contracts have been designated as cash flow hedges. The effective portion of the gain or loss on the derivative is

recorded in accumulated other comprehensive income to the extent effective and reclassified into earnings in the same period or periods

during which the transaction hedged by that derivative also affects earnings. The ineffective portion of the gain or loss on the derivative is

recorded in other expense, net. The ineffective portion of our cash flow foreign currency derivative instruments and the net gains or losses

reclassified from AOCI to earnings for cash flow hedges that had been discontinued because the forecasted transactions were not probable

of occurring were not material.

As of December 31, 2010, we expect to reclassify $3.9, net of taxes, of net losses on derivative instruments designated as cash flow hedges

from AOCI to earnings during the next 12 months.

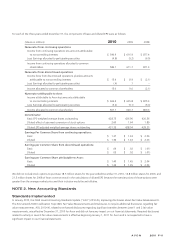

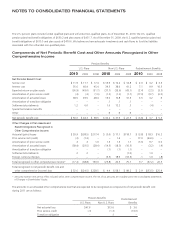

For the years ended December 31, 2010 and 2009, cash flow hedges and treasury lock agreements impacted AOCI as follows:

2010 2009

Net derivative losses at beginning of year, net of taxes

of $10.1 and $14.8 $(18.8) $(27.2)

Net losses on derivative instruments, net of taxes

of $0 and $1.1 – (2.3)

Reclassification of net gains to earnings, net of taxes

of $2.2 and $5.8 4.2 10.7

Net derivative losses at end of year, net of taxes

of $7.9 and $10.1 $(14.6) $(18.8)

We also use foreign exchange forward contracts to manage foreign currency exposure of intercompany loans. These contracts are not

designated as hedges for financial reporting purposes. The change in fair value of these contracts is immediately recognized in earnings and

substantially offsets the foreign currency impact recognized in earnings relating to the intercompany loans. During 2010, we recorded a loss

of $2.1 in other expense, net related to these undesignated foreign exchange forward contracts. Also during 2010, we recorded a gain of

$6.0 related to the intercompany loans, caused by changes in foreign currency exchange rates.

We have used foreign exchange forward contracts and foreign currency-denominated debt to hedge the foreign currency exposure related

to the net assets of foreign subsidiaries. Losses of $3.7 for 2010, $23.8 for 2009, and $33.6 for 2008, related to the effective portions of

these hedges were included in foreign currency translation adjustments within AOCI on the Consolidated Balance Sheets. During 2010 a loss

of $20.1 was reclassified from AOCI to discontinued operations due to the sale of Avon Japan.

A V O N 2010 F-21