Advance Auto Parts 2013 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2013 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

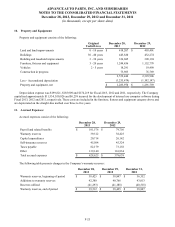

ADVANCE AUTO PARTS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

December 28, 2013, December 29, 2012 and December 31, 2011

(in thousands, except per share data)

F-23

was not significant due to the narrow margin between the lock rate and the underlying treasury rate. The Company did not

maintain any derivative financial instruments during the current fiscal year.

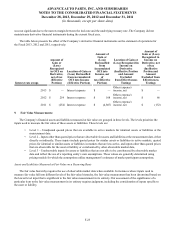

The table below presents the effect of the Company’s derivative financial instruments on the statement of operations for

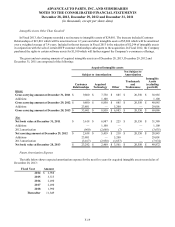

the Fiscal 2013, 2012 and 2011, respectively:

Interest rate swaps

Amount of

Gain or

(Loss)

Recognized

in OCI on

Derivative,

net of tax

(Effective

Portion)

Location of Gain or

(Loss) Reclassified

from Accumulated

OCI into Income

(Effective Portion)

Amount of

Gain or

(Loss)

Reclassified

from

Accumulated

OCI into

Income, net

of

tax (Effective

Portion)

Location of Gain or

(Loss) Recognized in

Income on

Derivative

(Ineffective Portion

and Amount

Excluded

from Effectiveness

Testing)

Amount of

Gain or (Loss)

Recognized in

Income on

Derivative, net

of tax

(Ineffective

Portion and

Amount

Excluded from

Effectiveness

Testing)

2013 $ — Interest expense $ —

Other (expense)

income, net $ —

2012 $ 254 Interest expense $ 108

Other (expense)

income, net $ 66

2011 $ (254) Interest expense $ (4,807)

Other (expense)

income, net $ (132)

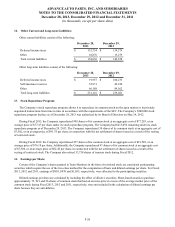

9. Fair Value Measurements:

The Company’s financial assets and liabilities measured at fair value are grouped in three levels. The levels prioritize the

inputs used to measure the fair value of these assets or liabilities. These levels are:

• Level 1 – Unadjusted quoted prices that are available in active markets for identical assets or liabilities at the

measurement date.

• Level 2 – Inputs other than quoted prices that are observable for assets and liabilities at the measurement date, either

directly or indirectly. These inputs include quoted prices for similar assets or liabilities in active markets, quoted

prices for identical or similar assets or liabilities in markets that are less active, and inputs other than quoted prices

that are observable for the asset or liability or corroborated by other observable market data.

• Level 3 – Unobservable inputs for assets or liabilities that are not able to be corroborated by observable market

data and reflect the use of a reporting entity’s own assumptions. These values are generally determined using

pricing models for which the assumptions utilize management’s estimates of market participant assumptions.

Assets and Liabilities Measured at Fair Value on a Recurring Basis

The fair value hierarchy requires the use of observable market data when available. In instances where inputs used to

measure fair value fall into different levels of the fair value hierarchy, the fair value measurement has been determined based on

the lowest level input that is significant to the fair value measurement in its entirety. Our assessment of the significance of a

particular item to the fair value measurement in its entirety requires judgment, including the consideration of inputs specific to

the asset or liability.