Advance Auto Parts 2013 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2013 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

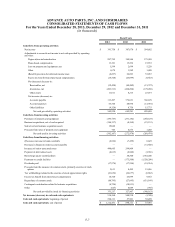

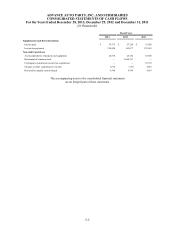

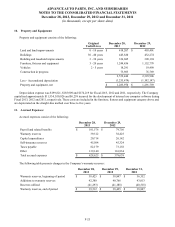

ADVANCE AUTO PARTS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

December 28, 2013, December 29, 2012 and December 31, 2011

(in thousands, except per share data)

F-15

Cost of Sales and Selling, General and Administrative Expenses

The following table illustrates the primary costs classified in each major expense category:

Cost of Sales SG&A

Total cost of merchandise sold including: Payroll and benefit costs for retail and corporate

- Freight expenses associated with moving Team Members;

merchandise inventories from our vendors to Occupancy costs of retail and corporate facilities;

our distribution center, Depreciation related to retail and corporate assets;

- Vendors incentives, and Advertising;

- Cash discounts on payments to vendors; Costs associated with our commercial delivery

Inventory shrinkage; program, including payroll and benefit costs,

Defective merchandise and warranty costs; and transportation expenses associated with moving

Costs associated with operating our distribution merchandise inventories from our retail store to

network, including payroll and benefit costs, our customer locations;

occupancy costs and depreciation; and Self-insurance costs;

Freight and other handling costs associated with Professional services;

moving merchandise inventories through our Other administrative costs, such as credit card

supply chain service fees, supplies, travel and lodging;

- From our distribution centers to our retail Closed store expense;

store locations, and Impairment charges;

- From certain of our larger stores which stock a GPI acquisition-related expenses; and

wider variety and greater supply of inventory (“HUB BWP acquisition-related expenses and integration costs.

stores”) and Parts Delivered Quickly warehouses

(“PDQ®s”) to our retail stores after the customer

has special-ordered the merchandise.

New Accounting Pronouncements

In July 2013, the Financial Accounting Standards Board, or FASB, issued ASU No. 2013-11 “Presentation of an

Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward

Exists.” Under ASU 2013-11 an entity is required to present an unrecognized tax benefit, or a portion of an

unrecognized tax benefit, in the financial statements as a reduction to a deferred tax asset for a net operating loss

carryforward, a similar tax loss, or a tax credit carryforward. If a net operating loss carryforward, a similar tax loss, or a

tax credit carryforward is not available at the reporting date, the unrecognized tax benefit should be presented in the

financial statements as a liability and should not be combined with deferred tax assets. ASU 2013-11 is effective for

fiscal years, and interim periods within those years, beginning after December 15, 2013. The adoption of this guidance

affects presentation only and, therefore, it is not expected to have a material impact on the Company’s consolidated

financial condition, results of operations or cash flows.

In February 2013, the FASB issued ASU No. 2013-02 “Comprehensive Income - Reporting of Amounts Reclassified Out

of Accumulated Other Comprehensive Income.” ASU 2013-02 is an amendment adding new disclosure requirements for items

reclassified out of accumulated other comprehensive income (“AOCI”). The amendment requires presentation of changes in

AOCI balances by component and significant items reclassified out of AOCI by component either (1) on the face of the

statement of operations or (2) as a separate disclosure in the notes to the financial statements. ASU 2013-02 is effective for

fiscal years beginning after December 15, 2012. The adoption of ASU 2013-02 had no impact on the Company’s consolidated

financial condition, results of operations or cash flows.