Advance Auto Parts 2004 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2004 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

|

|

26

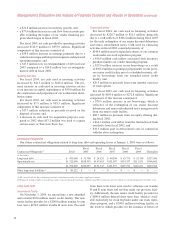

CreditRatings

AtJanuary1,2005,wehadacreditratingonoursenior

creditfacilityfromStandard&Poor’sofBB+andacredit

ratingofBa2fromMoody’sInvestorService.Thecurrent

pricinggridusedtodetermineourborrowingratesunder

our senior credit facility is based on such credit ratings.

If these credit ratings decline, our interest expense may

increase. Conversely, if these credit ratings increase, our

interestexpensemaydecrease.

Seasonality

Our business is somewhat seasonal in nature, with the

highestsalesoccurringinthespringandsummermonths.

Inaddition,ourbusinesscanbeaffectedbyweather

conditions. While unusually heavy precipitation tends to

soften sales as elective maintenance is deferred during

such periods, extremely hot or cold weather tends to

enhancesalesbycausingautomotivepartstofail.

RecentAccountingPronouncements

In April 2002, the FASB issued SFAS No. 145,

“Rescission of FASB Statements No. 4, 44 and 64,

Amendment of FASB Statement No. 13 and Technical

Corrections.” As a result of rescinding FASB Statement

No. 4, “Reporting Gains Losses from Extinguishment of

Debt,”gainsandlossesfromextinguishmentofdebtshould

beclassifiedasextraordinary itemsonlyiftheymeetthe

criteria in APB Opinion No. 30, “Reporting the Results

of Operations—Reporting the Effects of Disposal of a

Segment of a Business, and Extraordinary, Unusual and

Infrequently Occurring Events and Transactions.” This

statementalsoamendsFASBStatementNo.13,“Accounting

for Leases,” to eliminate an inconsistency between the

requiredaccountingforsale-leasebacktransactionsandthe

required accounting for certain lease modifications that

have economic effects that are similar to sale-leaseback

transactions. Additional amendments include changes to

otherexistingauthoritativepronouncementstomakevari-

ous technical corrections, clarify meanings or describe

their applicability under changed conditions. We adopted

SFASNo.145duringthefirstquarteroffiscal2003.For

thefiscalyearsended2004,2003and2002,werecorded

losses on the extinguishment of debt of $3,230, $47,288

and$16,822,respectively.

In July 2003 (as subsequently updated in November

2003),theFASBreleasedEmergingIssuesTaskForce,or

EITF,IssueNo.03-10,“ApplicationofIssueNo.02-16by

Resellers to Sales Incentives Offered to Customers by

Manufacturers.” This EITF addresses whether a reseller

should account for consideration received from a vendor

that is a reimbursement by the vendor for honoring the

vendor’s salesincentivesoffereddirectlytoconsumers in

accordancewiththeguidanceinEITFIssueNo.02-16.For

purposesofthisIssue,the“vendor’ssalesincentiveoffered

directly to consumers” is limited to a vendor’s incentive

(i) that can be tendered by a consumer at resellers that

accept manufacturer’s incentives in partial (or full) of

thepricechargedbytheresellerforthevendor’sproduct,

(ii)forwhichtheresellerreceivesadirectreimbursement

from the vendor (or a clearinghouse authorized by the

vendor)basedonthefaceamountoftheincentive,(iii)for

which the terms of reimbursement to the reseller for the

vendor’ssalesincentiveofferedtotheconsumermustnot

be influenced by or negotiated in conjunction with any

other incentivearrangementsbetweenthevendorandthe

resellerbut,rathermayonlybedeterminedbythetermsof

the incentive offered to consumers and (iv) whereby the

resellerissubjecttoanagencyrelationshipwith theven-

dor, whether expressed or implied, in the sales incentive

transaction between the vendor and the consumer. The

consensus is that sales incentives that meet all of such

criteriaarenotsubjecttotheguidanceinIssueNo.02-16.

The release is effectiveforfiscal periods beginningafter

November 25, 2003. We adopted this release during the

firstquarteroffiscal2004withnoimpactonourfinancial

positionorresultsofoperations.

InMay2004,theFASBissuedFASBStaffPosition,or

FSP, 106-2, “Accounting and Disclosure Requirements

Related to the Medicare Prescription Drug, Improvement

and Modernization Act of 2003.” FSP 106-2 addresses

the appropriate accounting and disclosure requirements

for companies that sponsor a postretirement health care

plan that provides prescription drug benefits. The new

guidance was deemed necessary as a result of the 2003

Medicare prescription law which includes a federal sub-

sidy for qualifying companies. The effective date of FSP

106-2isthefirstinterimorannualperiodbeginningafter

June15,2004.Wecompletedanegativeplanamendment

toeliminateoutpatientprescriptiondrugbenefitsfromour

postretirementplaneffectiveinthesecondquarteroffiscal

2004;therefore,theadoptionofFSP106-2hadnoimpact

on our financial position, results of operations or related

footnotedisclosure.

Management’sDiscussionandAnalysisofFinancialConditionandResultsofOperations(continued)