ADT 2000 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2000 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

THIRTY ONE

million. The increase in deferred income taxes is attributable

primarily to current utilization of deductions on restructuring, other

non-recurring charges and purchase accounting spending, other

timing differences between book and tax recognition of income and

expense, utilization of net operating loss and credit carryforwards,

and the tax benefits of stock option exercises.

The net change in working capital, net of the effects of acqui-

sitions and divestitures, was an increase of $91.7 million. The com-

ponents of this change are set forth in detail in the Consolidated

Statement of Cash Flows. The increase in working capital accounts

is attributable to the higher level of business activity in Fiscal 2000

as reflected in the increased sales over the prior year. We focus on

maximizing the cash flow from our operating businesses and

attempt to keep the working capital employed in the businesses to

the minimum level required for efficient operations.

In addition, we used $1,885.1 million to purchase our own

common shares. In November 1999, we announced the authoriza-

tion by our Board of Directors to reacquire up to 20 million Tyco com-

mon shares in the open market, which was completed during the

quarter ended March 31, 2000. In January 2000, the Board of Direc-

tors authorized the expenditure of up to an additional $2,000.0 mil-

lion to reacquire our shares, of which we have spent nearly $1,100.0

million through September 30, 2000. In addition, we repurchase

our own shares from time to time in the open market to satisfy cer-

tain stock-based compensation arrangements, such as the exercise

of stock options.

We received proceeds of $2,130.7 million from the issuance of

common shares by a subsidiary in the TyCom IPO and $355.3 mil-

lion from the exercise of common share options.

The source of the cash used for acquisitions was primarily an

increase in total debt and cash flows from operations. Goodwill and

other intangible assets were $16,332.6 million at September 30,

2000, compared to $12,158.9 million at September 30, 1999.

At September 30, 2000, our total debt was $10,999.0 million,

as compared to $10,122.2 million at September 30, 1999. This

increase resulted principally from borrowings under our commercial

paper program and net proceeds of approximately $565.9 million

from the issuance of Euro denominated private placement notes in

April 2000. For a full discussion of debt activity, see Note 4 to the

Consolidated Financial Statements.

Shareholders’ equity was $17,033.2 million, or $10.11 per share,

at September 30, 2000, compared to $12,369.3 million, or $7.32

per share, at September 30, 1999. The increase in shareholders’

equity was due primarily to net income of $4,519.9 million, an unre-

alized gain on available for sale securities of $1,075.7 million and

the issuance of a total of approximately 15.6 million common shares

valued at approximately $671.4 million for the acquisitions of GSI

and AFC Cable in November 1999. Total debt as a percent of total

capitalization (total debt and shareholders’ equity) was 39% at

September 30, 2000 and 45% at September 30, 1999. Net debt

(total debt less cash and cash equivalents) as a percent of total

capitalization was 35% at September 30, 2000 and 37% at

September 30, 1999.

On October 4, 2000, we entered into an agreement to acquire

InnerDyne, Inc. (“InnerDyne”), a manufacturer and distributor of

patented radial dilating access devices used in minimally invasive

medical surgical procedures. The purchase price is approximately

$180 million payable in Tyco common shares. InnerDyne will be

integrated within Tyco’s Healthcare business. We intend to account

for the acquisition as a purchase.

On October 6, 2000, we sold our ADT Automotive business to

Manheim Auctions, Inc., a wholly-owned subsidiary of Cox Enter-

prises, Inc., for approximately $1 billion in cash. The sale is

expected to generate a one-time pre-tax gain to Tyco in excess of

$300 million in the first quarter of Fiscal 2001.

On October 17, 2000, we acquired Mallinckrodt Inc.

(“Mallinckrodt”), a global healthcare company with products used

primarily for respiratory care, diagnostic imaging and pain relief. We

issued approximately 64.8 million common shares, valued at

approximately $3.2 billion, and assumed approximately $1.0 billion

in debt. Mallinckrodt is being integrated within Tyco’s Healthcare

business. We are accounting for the acquisition as a purchase.

On November 13, 2000, we agreed to acquire the Lucent Power

Systems (“LPS”) business unit of Lucent Technologies, Inc. for $2.5

billion in cash. LPS provides a full line of energy solutions and power

products for telecommunications service providers and for the com-

puter industry and will be integrated within the Electronics seg-

ment. LPS products include AC/DC and DC/DC switching power

supplies, batteries, power supplies and back-up power systems. The

acquisition is subject to customary regulatory approvals.

On November 17, 2000, we completed a private placement

offering of $4,657,500,000 principal at maturity of zero-coupon debt

securities due 2020 for aggregate net proceeds of approximately

$3,374,000,000. Each $1,000 principal amount at maturity security

was issued at 74.165% of principal amount at maturity, accretes at

a rate of 1.5% per annum and is convertible into 10.3014 Tyco com-

mon shares if certain conditions are met. We may be required to

repurchase the securities at the accreted value at the option of the

holders on November 17, 2001, 2003, 2005, 2007 or 2014. The pro-

ceeds of this offering will be used to finance the LPS acquisition and

to repay commercial paper.

On December 4, 2000, we agreed to acquire Simplex Time

Recorder Co. (“Simplex”) for approximately $1.15 billion in cash.

Simplex manufactures fire and security products and communica-

tions systems including control panels, detection devices and

system software. Simplex also installs, monitors and services fire

alarms, security systems and access control systems and will be

integrated within the Fire and Security Services segment. The

acquisition is subject to customary regulatory approvals.

We believe that our cash flow from operations, together with our

existing credit facilities and other credit arrangements, is adequate

to fund our operations.

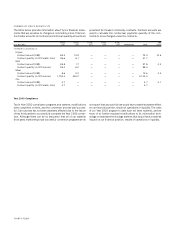

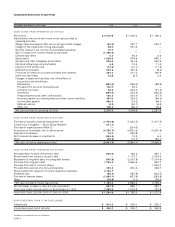

BACKLOG

At September 30, 2000, we had a backlog of unfilled orders of

approximately $8,214.8 million, compared to a backlog of approxi-

mately $7,581.1 million as of September 30, 1999. We expect that

approximately 86% of our backlog at September 30, 2000 will be

filled during the year ending September 30, 2001. Backlog by indus-

try segment is as follows:

SEPTEMBER 3 0 ,

(I N MILLI ONS) 2 0 0 0 1 9 9 9

Telecommunications $ 2 ,9 4 1 .7 $3,535.4

Electronics 2 ,3 3 5 .7 1,439.1

Flow Control Products and Services 1 ,7 1 1 .4 1,516.5

Fire and Security Services 1 ,1 3 4 .9 986.6

Healthcare and Specialty Products 9 1 .1 103.5

$ 8 ,2 1 4 .8 $7,581.1