TCF Bank 2011 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2011 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

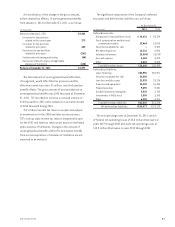

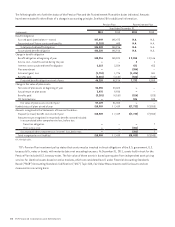

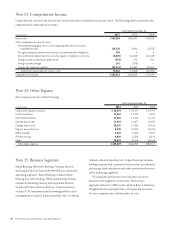

Prior service credits of the Postretirement Plan totaling

$29 thousand are included within accumulated other

comprehensive income at December 31, 2011 and are

expected to be recognized as components of net periodic

benefit cost during 2012.

The actuarial assumptions used in the Pension Plan

valuation are reviewed annually. The expected long-term

rate of return on plan assets is determined by reference

to historical market returns and future expectations. The

10-year average return of the index consistent with the

Pension Plan’s current investment strategy was 3.9%, net

of administrative expenses. Although past performance is

no guarantee of the future results, TCF is not aware of any

reasons why it should not be able to achieve the assumed

future average long-term annual returns of 1.5%, net of

administrative expenses, on plan assets over complete

market cycles. A 1% difference in the expected return on

plan assets would result in a $550 thousand change in net

periodic benefit cost.

The discount rate used to determine TCF’s Pension

Plan and Postretirement Plan benefit obligations as of

December 31, 2011 and December 31, 2010, was determined

by matching estimated benefit cash flows to a yield

curve derived from corporate bonds rated AA by Moody’s.

Bonds containing call or put provisions were excluded.

The average estimated duration of TCF’s Pension and

Postretirement Plans varied between seven and eight years.

Included within the net periodic benefit plan cost for the

Pension Plan are recognized actuarial gains and losses.

The decrease in the discount rate from 4.75% at December

31, 2010 to 4% at December 31, 2011 increased net periodic

pension cost by $2.4 million during 2011. The reduction of

the interest crediting rate from 4.5% at December 31, 2010

to 3.5% at December 31, 2011 and other interest crediting

assumption changes reduced net periodic pension cost

for 2011 by $3.7 million. Various plan participant census

changes decreased the 2011 net periodic pension cost by

$400 thousand.

Included in the net periodic benefit plan cost for the

Postretirement Plan are recognized actuarial gains and

losses. The Postretirement Plan change in actuarially

estimated cost per participant as of December 31, 2011

reduced net periodic benefit cost by $1.3 million. Actual

claims paid during 2011 totaled $453 thousand less than

expected, reducing net periodic benefit cost. The decrease

in the discount rate from 4.75% at December 31, 2010 to

4% at December 31, 2011 increased net periodic benefit

cost by $410 thousand. Various plan demographic changes

decreased the net periodic pension cost by $72 thousand.

For 2011, TCF is eligible to contribute up to $18 million

to the Pension Plan until the 2011 federal income tax return

extension due date under various IRS funding methods.

During 2011, TCF made no cash contributions to the Pension

Plan. TCF does not expect to be required to contribute

to the Pension Plan in 2012. TCF expects to contribute

$823 thousand to the Postretirement Plan in 2012. TCF

contributed $526 thousand and $528 thousand to the

Postretirement Plan for the years ended December 31, 2011

and 2010, respectively. TCF currently has no plans to pre-

fund the Postretirement Plan in 2012.

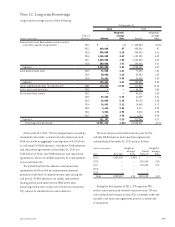

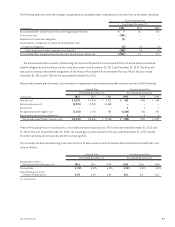

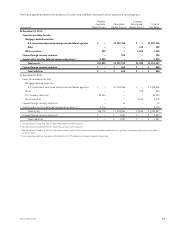

The following are expected future benefit payments

used to determine projected benefit obligations.

(In thousands)

Pension

Plan

Postretirement

Plan

2012 $ 4,288 $ 823

2013 3,646 799

2014 4,097 770

2015 3,182 738

2016 3,201 705

2017-2021 14,773 2,984

The following table presents assumed health care cost

trend rates for the Postretirement Plan at December 31,

2011 and 2010.

2011 2010

Health care cost trend rate assumed for next year 6.75% 7.50%

Final health care cost trend rate 5% 5%

Year that final health care trend rate is reached 2023 2023

Assumed health care cost trend rates have an effect on

the amounts reported for the Postretirement Plan. A 1%

change in assumed health care cost trend rates would have

the following effects.

1-Percentage-Point

(In thousands) Increase Decrease

Effect on total service and

interest cost components $ 19 $ (18)

Effect on postretirement

benefits obligations 354 (321)

88 TCF Financial Corporation and Subsidiaries