Seagate 2010 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2010 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

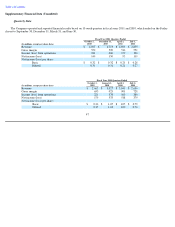

Table of Contents

be best served by hard disk drives based on the industry's ability to deliver reliable, energy efficient and cost effective mass storage devices.

Disk Drives for Enterprise Storage. We define enterprise storage as disk drives designed for mission critical applications and nearline

applications.

Mission critical applications are defined as applications that are vital to the operation of enterprises, requiring high performance, and high

reliability disk drives. We expect the market for mission critical enterprise storage solutions to continue to be driven by enterprises moving

network traffic to dedicated storage area networks in an effort to reduce network complexity and increase energy savings. We believe that this

transition will lead to an increased demand for more energy efficient, smaller form factor disk drives. These solutions are comprised principally

of high performance enterprise class disk drives with sophisticated firmware and communications technologies.

Nearline applications are defined as applications that are capacity-intensive and require high capacity and energy efficient disk drives

featuring lower costs per gigabyte. We expect such applications, which include storage for cloud computing and backup services, will continue

to grow and drive demand for disk drives designed with these attributes.

We believe the TAM for enterprise disk drives for the fiscal year 2011 was approximately 55 million units, an increase of 16% compared to

the prior fiscal year. We believe that the increase in the TAM from fiscal year 2010 was driven by enterprises moving network traffic to

dedicated storage area networks in an effort to reduce network complexity and increase energy savings.

SSD storage applications have been introduced as a potential alternative to redundant system startup or boot disk drives. In addition,

enterprises are gradually adopting SSDs in applications where rapid processing and/or energy efficiency is required. The timing of significant

adoption of SSDs is dependent on enterprises weighing the cost effectiveness and other benefits of mission critical enterprise disk drives against

the perceived performance benefits of SSDs.

Disk Drives for Client Compute. We define client compute applications as disk drives designed for the traditional desktop and mobile

compute applications. We believe that the client compute TAM for the fiscal year 2011 was approximately 483 million units, a decrease of 1%

compared to prior fiscal year. We believe that the increase in demand resulting from growing economies of certain countries and the continued

proliferation of digital content will drive the demand for the client compute market.

Disk Drives for Client Non-Compute. We define client non-compute applications as disk drives designed for consumer electronic devices

and disk drives used for external storage and network-attached storage (NAS). Disk drives designed for consumer electronic devices are

primarily used in applications such as DVRs that require a higher capacity, lower cost-per-

gigabyte storage solution. Disk drives for external and

NAS devices are designed for purposes such as personal data backup and portable external storage, and to augment storage capacity in the

consumer's current desktop, notebook, tablet or DVR. Client non-compute applications also include devices designed to display digital media in

the home theater. We believe the proliferation of high definition and media-rich digital content will continue to create increasing consumer

demand for higher storage solutions. As the proliferation of non-client compute applications that require minimal storage such as tablets

continues, SSDs could become more competitive within the client compute market in the future.

We believe the client non-compute TAM in the fiscal year 2011 was approximately 119 million units, an increase of 20% from the prior

fiscal year primarily due to the strength of the retail market in Asia Pacific during most of the fiscal year.

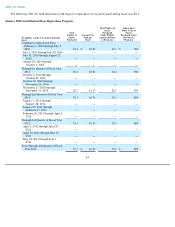

Industry Supply Balance

From time to time the industry has experienced periods of imbalance between supply and demand. To the extent that the disk drive industry

builds capacity based on expectations of demand that do not

50