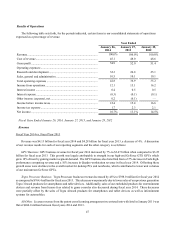

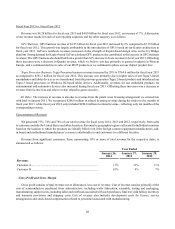

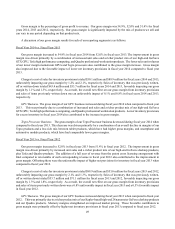

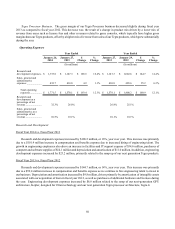

NVIDIA 2013 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2013 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

44

Both a qualitative and quantitative approach are applicable accounting standards for the assessment of goodwill

impairment. With the qualitative approach to testing goodwill for impairment, we perform an analysis evaluating factors

including, but not limited to, macro-economic conditions, market and industry conditions, the competitive environment,

the operational stability and overall financial performance of the reporting units, including cost factors and actual revenue

results. For reporting units in which the qualitative assessment concludes it is more likely than not that the fair value is more

than its carrying value, no further goodwill impairment testing is required.

For those reporting units where a significant change or event has occurred, where potential impairment indicators exist,

or for which we have not performed a quantitative assessment recently, we utilize a two-step quantitative assessment to

testing goodwill for impairment. The first step tests for possible impairment by applying a fair value-based test. The second

step, if necessary, measures the amount of such impairment by applying fair value-based tests to individual assets and

liabilities. We estimated the fair value of reporting units by weighing the results from the income approach and the market

approach. These valuation approaches consider a number of factors that include, but are not limited to, prospective financial

information, growth rates, terminal or residual values, discount rates and comparable multiples from publicly traded

companies in our industry and require us to make certain assumptions and estimates regarding industry economic factors

and the future profitability of our business.

When performing an income approach valuation, we incorporate the use of projected financial information and a

discount rate that are developed using market participant based assumptions to our discounted cash flow model. Our

estimates of discounted cash flow were based upon, among other things, certain assumptions about our expected future

operating performance, such as revenue growth rates, operating margins, risk-adjusted discount rates, and future economic

and market conditions. Our estimates may differ from actual cash flow due to, among other things, economic conditions,

changes to our business model or changes in operating performance. Additionally, certain estimates of discounted cash flow

involve businesses with limited financial history and developing revenue models, which increases the risk of differences

between the projected and actual performance. The long-term financial forecasts that we utilize represent the best estimate

that we have at this time and we believe that its underlying assumptions are reasonable. Significant differences between

our estimates and actual cash flow could materially affect our future financial results, which could impact our future estimates

of the fair value of our reporting unit.

During the fourth quarter of fiscal year 2014, we utilized a quantitative assessment to test goodwill impairment for all

three reporting units and concluded that there was no impairment, as the fair value of our GPU and Professional Solutions

reporting units significantly exceeded their carrying values and the fair value of our Tegra Processor reporting unit exceeded

its carrying value by 17%. As such, even if we applied a hypothetical 10% decrease to the fair value of each reporting unit,

it still would not have resulted in the fair value of our reporting units being less than their carrying values. As an overall

test of the reasonableness of estimated fair values of reporting units, we reconciled the combined fair value estimates of

our reporting units to our market capitalization as of the valuation date of October 27, 2013. The reconciliation confirmed

that the fair values were relatively representative of the market views when applying a reasonable control premium to the

market capitalization. However, any significant reductions in the actual amount of future cash flows realized by our reporting

units, reductions in the value of market comparables, or reductions in our market capitalization could impact future estimates

of the fair values of our reporting units. Such events could ultimately result in a charge to our earnings in future periods

due to the potential for a write-down of the goodwill associated with our reporting units.

In particular, the fair value of our Tegra reporting unit exceeded its carrying value by approximately 17%. The fair

value of this reporting unit was assessed using a combination of income and market approaches. The underlying assumptions

we used in assessing the fair value of the Tegra reporting unit include, but are not limited to, assumptions around future

revenue growth rates, gross margins, operating expense investment levels, overall market growth rates, our market share

of the overall market, and the appropriate discount rates to apply to future cash flows. If the actual future results of the Tegra

reporting unit do not achieve the levels we estimated in assessing its fair value, the fair value of the Tegra reporting unit

could decline. A future decline in the fair value of the Tegra reporting unit could result a charge to our earnings as a result

of a write-down of the value of the goodwill associated with that reporting unit.