Foot Locker 2004 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2004 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

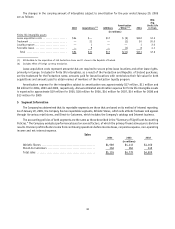

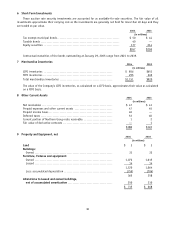

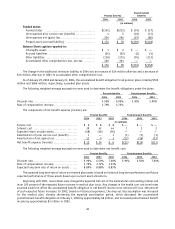

15 Other Liabilities

2004 2003

(in millions)

Pension benefits .......................................................... $130 $175

Postretirement benefits ................................................... 95 113

Straight-line rent liability.................................................. 77 67

Income taxes .............................................................. 29 62

Workers’ compensation / general liability reserves ......................... 11 12

Reserve for discontinued operations ....................................... 11 11

Repositioning and restructuring reserves .................................. 3 2

Fair value of derivatives ................................................... — 1

Unfavorable leases ........................................................ 3 —

Other ...................................................................... 17 15

$376 $458

16 Discontinued Operations

On January 23, 2001, the Company announced that it was exiting its 694-store Northern Group segment. During the

second quarter of 2001, the Company completed the liquidation of the 324 stores in the United States. On September 28,

2001, the Company completed the stock transfer of the 370 Northern Group stores in Canada, through one of its wholly

owned subsidiaries for approximately CAD$59 million (approximately US$38 million), which was paid in the form of a note

(the “Note”). Another wholly owned subsidiary of the Company was the assignor of the store leases involved in the

transaction and therefore retains potential liability for such leases. The net amount of the assets and liabilities of the

former operations was written down to the estimated fair value of the Note. The transaction was accounted for pursuant

to SEC Staff Accounting Bulletin Topic 5:E “Accounting for Divestiture of a Subsidiary or Other Business Operation,” as

a “transfer of assets and liabilities under contractual arrangement” as no cash proceeds were received and the

consideration comprised the Note, the repayment of which was dependent on the future successful operations of

the business.

An agreement in principle had been reached during December 2002 to receive CAD$5 million (approximately US$3

million) cash consideration in partial prepayment of the Note and accrued interest, and further, the Company agreed to

reduce the face value of the Note to CAD$17.5 million (approximately US$12 million). During the fourth quarter of 2002,

circumstances had changed sufficiently such that it became appropriate to recognize the transaction as an accounting

divestiture. Accordingly, the Note was recorded in the financial statements at its estimated fair value of CAD$16 million

(approximately US$10 million). On May 6, 2003, the amendments to the Note were executed and a cash payment of

CAD$5.2 million was received from the purchasers of the Northern Group, representing principal and interest through the

date of the amendment. On January 15, 2004, the Company received an additional payment of CAD$1 million, representing

a partial repayment of the Note. On August 20, 2004, the Company received a contingent payment of CAD$1 million, which

was based upon a certain transaction that occurred. As a result of the settlement of the contingent transaction, the

CAD$17.5 million Note was replaced with a new CAD$15.5 million note. The terms of the new note are substantially the

same as the May 6, 2003 Note, including the expiration date and interest payment terms.

Future adjustments, if any, to the carrying value of the Note will be recorded pursuant to SEC Staff Accounting Bulletin

Topic 5:Z:5, “Accounting and Disclosure Regarding Discontinued Operations,” which requires changes in the carrying value

of assets received as consideration from the disposal of a discontinued operation to be classified within continuing

operations. Interest income will also be recorded within continuing operations. The Company will recognize an impairment

loss when, and if, circumstances indicate that the carrying value of the Note may not be recoverable. Such circumstances

would include deterioration in the business, as evidenced by significant operating losses incurred by the purchaser or

nonpayment of an amount due under the terms of the Note. The purchaser has made all payments required under the terms

of the Note, however the business has sustained unexpected operating losses during the past fiscal year. The Company

has evaluated the projected performance of the business and will continue to monitor its results during the coming year.

At January 29, 2005 and January 31, 2004, US$1 million and US$2 million, respectively, are classified as a current

receivable, with the remainder classified as long term within other assets in the accompanying Consolidated Balance Sheets.

All scheduled principal and interest payments have been received timely and in accordance with the terms of the Note.

40