Food Lion 2012 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2012 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

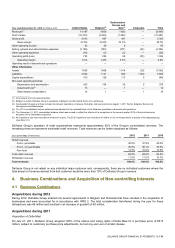

DELHAIZE GROUP FINANCIAL STATEMENTS ’12 // 81

Non-derivative Financial Assets

Delhaize Group classifies its non-derivative financial assets (hereafter “financial assets”) within the scope of IAS 39 Financial

Instruments: Recognition and Measurement into the following categories: held-to-maturity, loans and receivables and available-

for-sale. Delhaize Group currently holds no financial assets that would be classified as measured at fair value through profit or

loss. The Group determines the classification of its financial assets at initial recognition.

These financial assets are initially recorded at fair value plus transaction costs that are directly attributable to the acquisition or

issuance of the financial assets.

Loans and receivables: Financial assets with fixed or determinable payments that are not quoted in an active market are

classified as loans and receivables. Such financial assets are subsequent to initial recognition carried at amortized cost

using the effective interest rate method. Gains and losses are recognized in the income statement when the loans and

receivables are derecognized or impaired and through the amortization process. The Group’s loans and receivables

comprise “Other financial assets” (see Note 12), “Receivables” (see Note 14) and “Cash and cash equivalents” (see Note

15).

Trade receivables are subsequently measured at amortized cost less a separate impairment allowance. The allowance for

impairment of trade receivables is established (on a separate allowance account) when there is objective evidence that the

Group will not be able to collect all amounts due according to the original terms of the receivables and the amount of the loss

is recognized in the income statement within “Selling, general and administrative expenses.” Impaired trade receivables are

derecognized when they are determined to be uncollectible.

Available-for-sale investments: Available-for-sale investments are financial assets that are either designated in this category

or not classified in any of the other categories. After initial measurement, available-for-sale investments are measured at fair

value with unrealized gains or losses recognized directly in OCI, until the investment is derecognized or impaired, at which

time the cumulative gain or loss recorded in the available-for-sale reserve is recognized in the income statement as a

reclassification adjustment.

Delhaize Group mainly holds quoted investments and the fair value of these are predominately based on current bid prices

(see further Note 10.1). The Group monitors the liquidity of the quoted investments to identify inactive markets, if any. In a

very limited number of cases, e.g., if the market for a financial asset is not active (and for unlisted securities), the Group

establishes fair value by using valuation techniques making maximum use of market inputs, including broker prices from

independent parties, and relying as little as possible on entity-specific inputs, in which case the Group ensures that they are

consistent with the fair value measurement objective and is consistent with any other market information that is available.

For available-for-sale financial assets, the Group assesses at each balance sheet date whether there is objective evidence

that an investment or a group of investments is impaired. For investments in debt instruments, the impairment is assessed

based on the same criteria as financial assets carried at amortized cost (see above “Loans and receivables”). Interest

continues to be accrued at the original effective interest rate on the reduced carrying amount of the asset. If, in a subsequent

year, the fair value of a debt instrument increases and the increase can be objectively related to an event occurring after the

impairment loss was recognized in the income statement, the impairment loss is reversed through the income statement. For

investments in equity instruments the objective evidence for impairment includes a significant or prolonged decline in the fair

value of the investment below its costs. Where there is evidence of impairment, the cumulative loss – measured as the

difference between the acquisition cost and the current fair value, less any impairment loss on that investment previously

recognized in the income statement – is removed from equity and recognized in the income statement. Impairment losses on

equity investments are not reversed through the income statement. Increases in their fair value after impairment are

recognized directly in OCI.

Available-for-sale financial assets are included in “Investments in securities” (see Note 11). They are classified as non-

current assets except for investments with a maturity date less than 12 months from the balance sheet date.

Financial assets are derecognized when the rights to receive cash flows from the financial assets have expired, or if the Group

transferred the financial asset to another party and does not retain control or substantially all risks and rewards of the financial

asset.

Non-derivative Financial Liabilities

IAS 39 Financial Instruments: Recognition and Measurement contains two categories for non-derivative financial liabilities

(hereafter “financial liabilities”): financial liabilities at fair value through profit or loss and financial liabilities measured at amortized

cost. Delhaize Group mainly holds financial liabilities measured at amortized cost that are included in “Debts,” “Borrowings,”

“Accounts payable” and “Other liabilities.” In addition, the Group issued financial liabilities, which are part of a designated fair

value hedge relationship (see Note 19).

All financial liabilities are recognized initially at fair value, plus, for instruments not at fair value through profit or loss, any directly

attributable transaction costs.