Food Lion 2012 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2012 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

142 // DELHAIZE GROUP FINANCIAL STATEMENTS’12

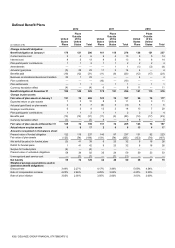

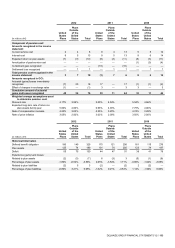

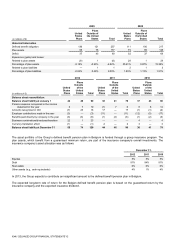

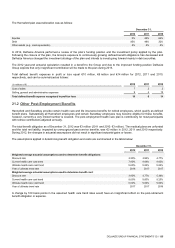

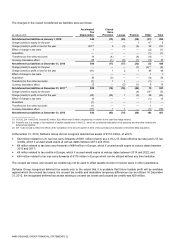

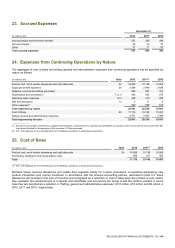

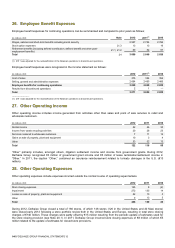

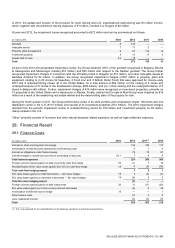

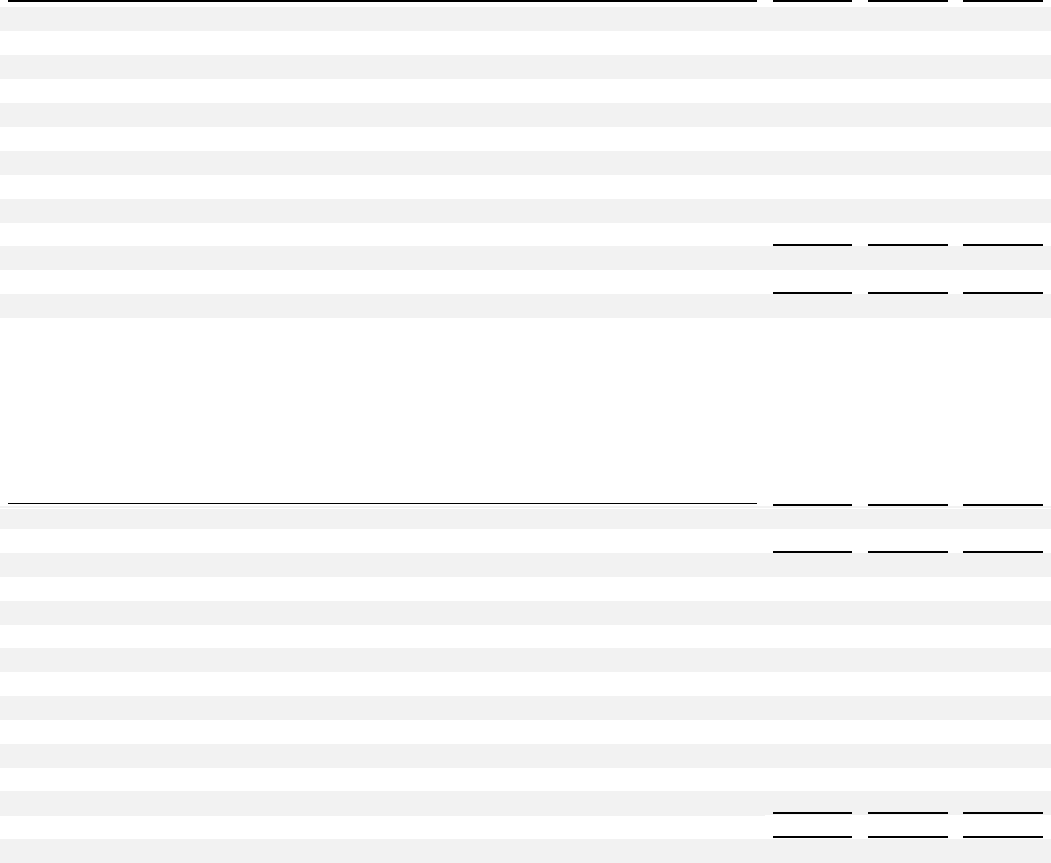

22. Income Taxes

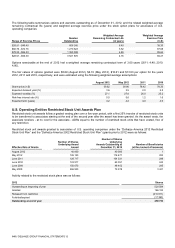

The major components of income tax expense for 2012, 2011 and 2010 were:

(in millions of €)

2012

2011

2010

Continuing operations

Current tax

110

103

17(1)

Taxes related to prior years recorded in the current year

(57)(2)

5

(2)

Utilization of previously unrecognized tax losses and tax credits

—

(1)

—

Other (current tax related)

2

—

—

Deferred tax

(62)

52

226(1)

Deferred taxes related to prior years recorded in the current year

6

(5)

3

Recognition of deferred tax on previously unrecognized tax losses and tax credits

(6)

(2)

—

Derecognition of previously recorded deferred tax assets

18

3

2

Deferred tax expense relating to changes in tax rates or the imposition of new taxes(3)

13

1

(1)

Total income tax expense from continuing operations

24

156

245

Total income tax expense from discontinued operations

(2)

—

—

Total income tax expense from continuing and discontinued operations

22

156

245

_______________

(1) In 2010, current tax decreased and deferred tax increased primarily due to a change in tax treatment of capital expenditures in the U.S., which are considered

deductible for tax purposes and therefore increase the deferred tax liabilities.

(2) Primarily related to the resolution of several tax matters in the U.S. which resulted in the recognition of an income tax benefit.

(3) In December 2012, the Serbian government enacted an increase in tax rate from 10 to 15%, effective as from January 1, 2013.

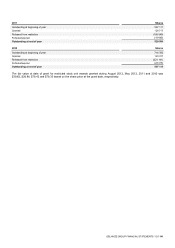

Profit before taxes can be reconciled with net profit as follows:

(in millions of €)

2012

2011(1)

2010

Continuing operations

149

633

821

Discontinued operations

(24)

(2)

(1)

Total profit before taxes

125

631

820

Continuing and discontinued operations

Current tax

109

103

17(2)

Taxes related to prior years recorded in the current year

(57)(3)

5

(2)

Utilization of previously unrecognized tax losses and tax credits

—

(1)

—

Other (current tax related)

2

—

—

Deferred tax

(63)

52

226(2)

Deferred taxes related to prior years recorded in the current year

6

(5)

3

Recognition of deferred tax on previously unrecognized tax losses and tax credits

(6)

(2)

—

Derecognition of previously recorded deferred tax assets

18

3

2

Deferred tax expense relating to changes in tax rates or the imposition of new taxes(4)

13

1

(1)

Total income tax expense from continuing and discontinued operations

22

156

245

Net profit

103

475

575

______________

(1) 2011 was adjusted for the reclassification of the Albanian operations to discontinued operations.

(2) In 2010, current tax decreased and deferred tax increased primarily due to a change in tax treatment of capital expenditures in the U.S., which are considered

deductible for tax purposes and therefore increase the deferred tax liabilities.

(3) Primarily related to the resolution of several tax matters in the U.S. which resulted in the recognition of an income tax benefit.

(4) In December 2012, the Serbian government enacted an increase in tax rate from 10 to 15%, effective as from January 1, 2013.