Cincinnati Bell 2012 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2012 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Form 10-K Part II Cincinnati Bell Inc.

for the asset or liability (i.e., interest rates, yield curves, etc.), and inputs that are derived principally from or

corroborated by observable market data by correlation or other means (market corroborated inputs); and

Level 3 — Unobservable inputs that reflect management’s determination of assumptions that market

participants would use in pricing the asset or liability. These inputs are developed based on the best

information available, including our own data.

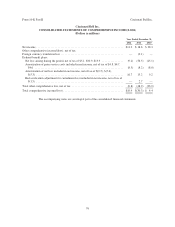

Foreign Currency Translation and Transactions — The financial position of foreign subsidiaries is

translated at the exchange rates in effect at the end of the period, while revenues and expenses are translated at

average rates of exchange during the period. Gains or losses from translation of foreign operations where the

local currency is the functional currency are included as components of accumulated other comprehensive

income/(loss). Gains and losses arising from foreign currency transactions are recorded in other income

(expense) in the period incurred.

2. Recently Issued Accounting Standards

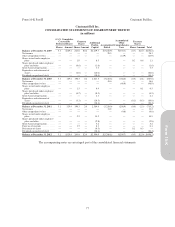

In February 2013, the FASB amended the guidance in ASC 220 on comprehensive income. The new

guidance will require additional information to be disclosed about the amounts reclassified out of accumulated

other comprehensive income by the respective line items of net income, but only if the amount reclassified is

required under U.S. GAAP to be reclassified in their entirety to net income. For other amounts that are not

required under U.S. GAAP to be reclassified in their entirety to net income, cross references to other disclosures

will be required. We will be required to adopt this new guidance beginning with our interim financial statements

for the three months ended March 31, 2013.

In July 2012, the FASB amended the guidance in ASC 350-30 on testing indefinite-lived intangible assets,

other than goodwill, for impairment. Under the revised guidance, an entity testing an indefinite-lived intangible

asset for impairment has the option of performing a qualitative assessment before performing quantitative tests.

If the entity determines, on the basis of qualitative factors, that the fair value of the indefinite-lived intangible

asset is not more likely than not impaired, the entity would not need to perform the quantitative tests. We adopted

this guidance for the year ended December 31, 2012. The adoption of this guidance did not have a material

impact on the Company’s financial statements.

In September 2011, the FASB amended the guidance in ASC 350-20 on testing goodwill for impairment.

Under the revised guidance, entities testing goodwill for impairment have the option of performing a qualitative

assessment before calculating the fair value of the reporting unit. If entities determine, on the basis of qualitative

factors, that the fair value of the reporting unit is more likely than not less than the carrying amount, the two-step

impairment test would be required. The Company adopted this guidance beginning with its interim financial

statements for the three months ended March 31, 2012. The adoption of this accounting standard did not have a

material impact on the Company’s financial statements.

In June 2011, the FASB issued new guidance under ASC 220 regarding the presentation of comprehensive

income in financial statements. An entity has the option to present the components of net income and other

comprehensive income (loss) either in a single continuous statement or in two separate but consecutive

statements. In March 2012, we adopted this accounting standard by presenting a separate statement of other

comprehensive income (loss) in our financial statements.

3. Acquisitions and Dispositions

Acquisition of Cyrus Networks, LLC

On June 11, 2010, the Company purchased Cyrus Networks, LLC (“Cyrus Networks”), a data center

operator based in Texas, for approximately $526 million, net of cash acquired, which was subsequently merged

into its subsidiary CyrusOne. The purchase of Cyrus Networks was accounted for as a business combination

under the acquisition method. Management completed the purchase price allocation early in 2011.

85

Form 10-K