Cincinnati Bell 2012 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2012 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Form 10-K Part II Cincinnati Bell Inc.

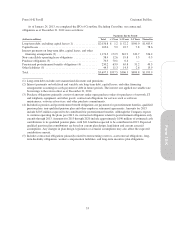

Reviewing the Carrying Values of Long-Lived Assets — Depreciation of our Wireline telephone plant is

determined on a straight-line basis using the group depreciation method. Depreciation of other property, except

for leasehold improvements, is based on the straight-line method over the estimated economic useful life.

Depreciation of leasehold improvements is based on a straight-line method over the lesser of the economic useful

life or term of the lease, including option renewal periods if renewal of the lease is reasonably assured. Repair

and maintenance expense items are charged to expense as incurred.

The useful lives of plant and equipment are estimated in order to determine the amount of depreciation

expense to be recorded during any reporting period. The majority of Wireline’s plant and equipment is

depreciated using the group method, which develops a depreciation rate annually based on the average useful life

of a specific group of assets rather than for each individual asset as would be utilized under the unit method. The

estimated life of the group changes as the composition of the group of assets and their related lives change. Such

estimated life of the group is based on historical experience with similar assets, as well as taking into account

anticipated technological or other changes.

If technological changes were to occur more rapidly than anticipated, the useful lives assigned to these

assets may need to be shortened, resulting in the recognition of increased depreciation expense in future periods.

Likewise, if the anticipated technological or other changes occur more slowly than expected, the life of the group

could be extended based on the life assigned to new assets added to the group. This could result in a reduction of

depreciation expense in future periods. Competition from new or more cost effective technologies could affect

our ability to generate cash flow from our network-based services. This competition could ultimately result in an

impairment of certain of our tangible or intangible assets. This could have a substantial impact on our future

operating results. A one-year change in the useful life of these assets would increase or decrease annual

depreciation expense by approximately $30 million.

Management reviews the carrying value of long-lived assets, other than goodwill and indefinite-lived

intangible assets discussed above, when events or changes in circumstances indicate that the carrying amount of

the assets may not be recoverable. An impairment loss is recognized when the estimated future undiscounted

cash flows expected to result from the use of an asset (or group of assets) and its eventual disposition is less than

its carrying amount. An impairment loss is measured as the amount by which the asset’s carrying value exceeds

its estimated fair value.

In 2012, management identified impairment indicators for a customer relationship intangible and long-lived

assets primarily associated with the 2007 GramTel acquisition. We performed step one of the impairment tests

utilizing cash flow projections from our most recent long-term business plan and other updated assumptions.

Management engaged a third-party valuation specialist to assist with the Company’s estimation of the fair value

of these assets.

Management estimated the fair value of the customer relationship using the income approach, which

discounted the expected earnings attributable to current customer contracts, and included estimates of future

expenses, capital expenditures and a discount rate of 12%. Management estimated the fair value of the customer

relationship intangible to be $2.8 million, resulting in an asset impairment of $1.5 million. The fair value of other

long-lived assets, primarily leasehold improvements, was estimated at $2.4 million, resulting in an impairment

loss of $11.8 million. Both fair value estimates are deemed Level 3 measurements within the fair value hierarchy

due to the significance of unobservable inputs utilized in these measurements. For the year ended December 31,

2012, impairment losses of $13.3 million were recognized in the Data Center Colocation segment.

During 2012, management also identified impairment indicators for an out-of-territory fiber network.

Management estimated the fair value of this asset using an income approach which discounted the expected

earnings attributable to current customer contracts, and included estimates of future expenses and a discount rate

of 12%. The fair value of this asset was estimated at $0.4 million, resulting in an impairment loss of $0.5 million.

This fair value estimate was deemed a Level 3 measurement within the fair value hierarchy due to the

significance of unobservable inputs utilized in these measurements. This impairment loss was recognized in the

59

Form 10-K