Albertsons 2008 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2008 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

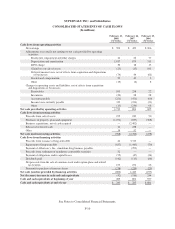

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

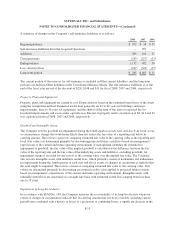

nonfinancial liabilities that are recognized or disclosed at fair value in the financial statements on a nonrecurring

basis. FSP 157-2 did not permit companies to defer recognition and disclosure requirements for financial assets

and financial liabilities or for nonfinancial assets and nonfinancial liabilities that are remeasured at least

annually. SFAS No. 157 is effective for financial assets and financial liabilities and for nonfinancial assets and

nonfinancial liabilities that are remeasured at least annually for the Company’s fiscal year beginning

February 24, 2008. The Company will defer adoption of SFAS No. 157 for one year for nonfinancial assets and

nonfinancial liabilities that are recognized or disclosed at fair value in the financial statements on a nonrecurring

basis. The Company is evaluating the effect the implementation of SFAS No. 157 will have on the consolidated

financial statements.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial

Liabilities–Including an amendment of FASB Statement No. 115.” SFAS No. 159 permits companies to choose,

at specified election dates, to measure eligible financial instruments and other financial assets and liabilities at

fair value. Unrealized gains and losses on items for which the fair value option has been elected should be

reported in earnings at each subsequent reporting date. The fair value option is applied instrument by instrument,

is irrevocable and is applied only to entire instruments and not to portions of instruments. SFAS No. 159 is

effective for the Company’s fiscal year beginning February 24, 2008, with early adoption permitted. SFAS

No. 159 is not expected to have a material effect on the consolidated financial statements.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS

No. 141(R)”). SFAS No. 141(R) expands the definition of a business combination and requires the fair value of

the purchase price of an acquisition, including the issuance of equity securities, to be determined on the

acquisition date. SFAS No. 141(R) also requires that all assets, liabilities, contingent considerations and

contingencies of an acquired business be recorded at fair value at the acquisition date. In addition, SFAS

No. 141(R) requires that acquisition costs generally be expensed as incurred, restructuring costs generally be

expensed in periods subsequent to the acquisition date and changes in accounting for deferred tax asset valuation

allowances and acquired income tax uncertainties after the measurement period impact income tax expense.

SFAS No. 141(R) is effective for the Company’s fiscal year beginning March 1, 2009 on a prospective basis for

all business combinations for which the acquisition date is on or after the effective date of SFAS No. 141(R),

with the exception of the accounting for adjustments to income tax-related amounts, which is applied to

acquisitions that closed prior to the effective date of SFAS No. 141(R). The Company is evaluating the effect the

implementation of SFAS No. 141(R) will have on the consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial

Statements, an Amendment of ARB No. 51.” SFAS No. 160 changes the accounting and reporting for minority

interests such that minority interests will be recharacterized as noncontrolling interests and will be required to be

reported as a component of equity, and requires that purchases or sales of equity interests that do not result in a

change in control be accounted for as equity transactions and, upon a loss of control, requires the interest sold, as

well as any interest retained, to be recorded at fair value with any gain or loss recognized in earnings. SFAS

No. 160 is effective for the Company’s fiscal year beginning March 1, 2009, with early adoption prohibited. The

Company is evaluating the effect the implementation of SFAS No. 160 will have on the consolidated financial

statements.

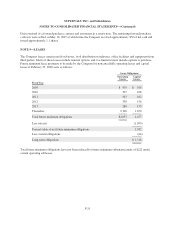

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging

Activities.” SFAS No. 161 amends and expands the disclosure requirements of SFAS No. 133 for derivative

instruments and hedging activities. SFAS No. 161 is effective for the Company’s fiscal year beginning March 1,

2009, with early adoption permitted. SFAS No. 161 does not impact the consolidated financial statements and the

Company is evaluating the effect the implementation will have on the Notes to Consolidated Financial

Statements.

F-18