eBay 2005 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2005 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

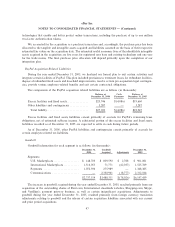

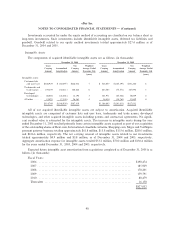

eBay Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Ì (Continued)

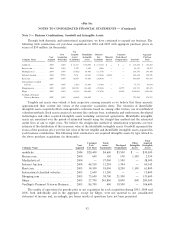

Recent Accounting Pronouncements

Share-Based Payments

In December 2004, the FASB issued Statement of Financial Accounting Standards No. 123 (revised

2004), ""Share-Based Payment'' (FAS 123R) that addresses the accounting for share-based payment

transactions in which an enterprise receives employee services in exchange for either equity instruments of the

enterprise or liabilities that are based on the fair value of the enterprise's equity instruments or that may be

settled by the issuance of such equity instruments. The statement eliminates the ability to account for share-

based compensation transactions, as we do currently, using the intrinsic value method prescribed by

Accounting Principles Board, or APB, Opinion No. 25, ""Accounting for Stock Issued to Employees,'' and

generally requires that such transactions be accounted for using a fair-value-based method and recognized as

expenses in our consolidated statement of income. The statement requires companies to assess the most

appropriate model to calculate the value of the options. We currently use the Black-Scholes option pricing

model to value options and are currently assessing which model we may use in the future under the new

statement and may deem an alternative model to be more appropriate. The use of a different model to value

options may result in a different fair value than the use of the Black-Scholes option pricing model. In addition,

there are a number of other requirements under the new standard that would result in different accounting

treatment than currently required. These differences include, but are not limited to, the accounting for the tax

benefit on employee stock options and for stock issued under our employee stock purchase plan, and the

presentation of these tax benefits within the consolidated statement of cash flows. In addition to the

appropriate fair value model to be used for valuing share-based payments, we will also be required to

determine the transition method to be used at date of adoption. The allowed transition methods are the

prospective and retroactive adoption alternatives. The prospective method requires that compensation expense

be recorded for all unvested stock options and restricted stock at the beginning of the first quarter of adoption

of FAS 123R, while the retroactive method requires companies to record compensation expense for all

unvested stock options and restricted stock beginning with the first disclosed period restated.

In April 2005, the Securities and Exchange Commission announced the adoption of a new rule that

amends the effective date of FAS 123R. The effective date of the new standard under these new rules for our

consolidated financial statements is January 1, 2006. Adoption of this statement will have a significant impact

on our consolidated financial statements as we will be required to expense the fair value of our stock option

grants and stock purchases under our employee stock purchase plan rather than disclose the impact on our

consolidated net income within our footnotes, as is our current practice (see ""The Company and Summary of

Significant Accounting Policies'').

The amounts disclosed within our footnotes are not necessarily indicative of the amounts that will be

expensed upon the adoption of FAS 123R. We expect the compensation charges under FAS 123R to reduce

earnings per diluted share by approximately $0.16 to $0.17 per share for the year ending December 31, 2006.

Compensation expense calculated under FAS 123R may differ from amounts currently disclosed within our

footnotes and may also differ from our expectations based on changes in the fair value of our common stock,

changes in the number of options granted or the terms of such options, the treatment of tax benefits and

changes in interest rates or other factors. In addition, upon adoption of FAS 123R, we may choose to use a

different valuation model to value the compensation expense associated with employee stock options and stock

purchases under our employee stock purchase plan.

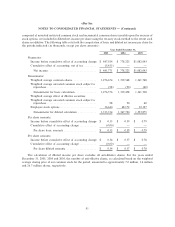

Note 2 Ì Net Income Per Share:

Basic net income per share is computed by dividing the net income for the period by the weighted average

number of common shares outstanding during the period. Diluted net income per share is computed by

dividing the net income for the period by the weighted average number of shares of common stock and

potentially dilutive common stock outstanding during the period. Potentially dilutive common stock,

90