UPS 2008 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2008 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

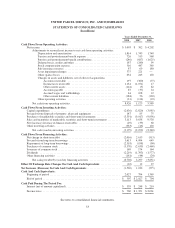

The following is a general description of the valuation methodologies used for financial assets and liabilities

measured at fair value, including the general classification of such assets and liabilities pursuant to the valuation

hierarchy.

Derivative Contracts—Our foreign currency, interest rate, and energy derivatives are largely comprised

of over-the-counter derivatives, which are primarily valued using pricing models that rely on market

observable inputs such as yield curves, currency exchange rates, and commodity forward prices, and

therefore are classified as Level 2.

Marketable Securities—Marketable securities utilizing Level 1 inputs include active exchange-traded

equity securities and equity index funds, and most U.S. Government debt securities, as these securities all

have quoted prices in active markets. Marketable securities utilizing Level 2 inputs include non-auction rate

asset-backed securities, corporate bonds, and municipal bonds. These securities are valued using market

corroborated pricing, matrix pricing, or other models that utilize observable inputs such as yield curves.

We have classified our auction rate securities portfolio as utilizing Level 3 inputs, as their valuation

requires substantial judgment and estimation of factors that are not currently observable in the market due to

the lack of trading in the securities. These valuations may be revised in future periods as market conditions

evolve. These securities were valued as of December 31, 2008 considering several factors, including the

credit quality of the securities, the rate of interest received since the failed auctions began, the yields of

securities similar to the underlying auction rate securities, and the input of broker-dealers in these securities.

Other Investments—Financial assets and liabilities utilizing Level 3 inputs include our holdings in

certain investment partnerships. These partnership holdings do not have any quoted prices, nor can they be

valued using inputs based on observable market data. These investments are valued internally using a

discounted cash flow model based on each partnership’s financial statements and cash flow projections.

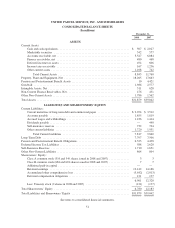

Depreciation, Residual Value, and Impairment of Fixed Assets—As of December 31, 2008, we had $18.265

billion of net fixed assets, the most significant category of which is aircraft. In accounting for fixed assets, we

make estimates about the expected useful lives and the expected residual values of the assets, and the potential

for impairment based on the fair values of the assets and the cash flows generated by these assets.

In estimating the lives and expected residual values of aircraft, we have relied upon actual experience with

the same or similar aircraft types. Subsequent revisions to these estimates could be caused by changes to our

maintenance program, changes in the utilization of the aircraft, governmental regulations on aging aircraft, and

changing market prices of new and used aircraft of the same or similar types. We periodically evaluate these

estimates and assumptions, and adjust the estimates and assumptions as necessary. Adjustments to the expected

lives and residual values are accounted for on a prospective basis through depreciation expense.

In accordance with the provisions of FAS 144, we review long-lived assets for impairment when

circumstances indicate the carrying amount of an asset may not be recoverable based on the undiscounted future

cash flows of the asset. If the carrying amount of the asset is determined not to be recoverable, a write-down to

fair value is recorded. Fair values are determined based on quoted market values, discounted cash flows, or

external appraisals, as applicable. We review long-lived assets for impairment at the individual asset or the asset

group level for which the lowest level of independent cash flows can be identified. The circumstances that would

indicate potential impairment may include, but are not limited to, a significant change in the extent to which an

asset is utilized, a significant decrease in the market value of an asset, and operating or cash flow losses

associated with the use of the asset. In estimating cash flows, we project future volume levels for our different air

express products in all geographic regions in which we do business. Adverse changes in these volume forecasts,

or a shortfall of our actual volume compared with our projections, could result in our current aircraft capacity

exceeding current or projected demand. This situation would lead to an excess of a particular aircraft type,

resulting in an aircraft impairment charge or a reduction of the expected life of an aircraft type (thus resulting in

increased depreciation expense).

We continually monitor our aircraft fleet utilization in light of current and projected volume levels, aircraft

fuel prices, and other factors. Changes in any of these factors, including a continuation of the rapid economic

44