Tyson Foods 2006 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2006 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

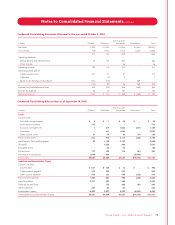

which are not discounted and are exclusive of claims against third

parties, are adjusted periodically as assessment efforts progress or

additional information becomes available. The Company expenses

amounts for administering or litigating claims as incurred. Accruals

for legal proceedings are included in Other current liabilities in the

Consolidated Balance Sheets.

• Freight Expense: Freight expense associated with products

shipped to customers is recognized in cost of sales.

• Advertising and Promotion Expenses: Advertising and promotion

expenses are charged to operations in the period incurred. Advertis-

ing and promotion expenses for fiscal years 2006, 2005 and 2004

were $493 million, $456 million and $465 million, respectively.

• Use of Estimates: The consolidated financial statements are pre-

pared in conformity with accounting principles generally accepted

in the United States, which require management to make estimates

and assumptions that affect the amounts reported in the consoli-

dated financial statements and accompanying notes. Actual results

could differ from those estimates.

• Recently Issued Accounting Standards and Regulations:

In March 2005, the FASB issued FIN 47. See Note 2, “Change in

Accounting Principles” of the Notes to Consolidated Financial

Statements for further discussion.

In September 2005, the Emerging Issues Task Force (EITF) reached a

consensus on Issue No. 04-13, “Accounting for Purchases and Sales

of Inventory with the Same Counterparty.” The issues were the

circumstances under which two or more inventory purchase and

sales transactions with the same counterparty should be viewed

as a single exchange transaction within the scope of Accounting

Principles Board Opinion 29, “Accounting for Nonmonetary Trans-

actions” and circumstances under which nonmonetary exchanges

of inventory within the same line of business should be recognized

at fair value. The Company adopted EITF Issue No. 04-13 in the third

quarter of fiscal 2006. The adoption of this Issue did not have a

material impact on the Company’s consolidated financial statements.

In June 2006, the FASB issued Interpretation No. 48, “Accounting for

Uncertainty in Income Taxes,” an interpretation of FASB Statement

No. 109 (FIN 48). FIN 48 prescribes a recognition threshold and

measurement attribute for the financial statement recognition

and measurement of a tax position taken or expected to be taken

in a tax return. FIN 48 also provides guidance on derecognition,

classification, interest and penalties, accounting in interim periods,

disclosure and transition. FIN 48 is effective for fiscal years begin-

ning after December 15, 2006; therefore the Company expects to

adopt FIN 48 at the beginning of fiscal 2008. The Company is cur-

rently in the process of evaluating the potential impact of FIN 48.

In September 2006, the FASB issued Statement of Financial

Accounting Standards No. 157, “Fair Value Measurements” (SFAS

No. 157). SFAS No. 157 provides guidance for using fair value to mea-

sure assets and liabilities. This standard also responds to investors’

requests for expanded information about the extent to which

companies measure assets and liabilities at fair value, the informa-

tion used to measure fair value and the effect of fair value measure-

ments on earnings. SFAS No. 157 applies whenever other standards

require (or permit) assets or liabilities to be measured at fair value.

The standard does not expand the use of fair value in any new

circumstances. SFAS No. 157 is effective for financial statements

issued for fiscal years beginning after November 15, 2007, and

interim periods within those fiscal years; therefore, the Company

expects to adopt SFAS No. 157 at the beginning of fiscal 2009. The

Company is currently in the process of evaluating the potential

impact of SFAS No. 157.

In September 2006, the FASB issued Statement of Financial Account-

ing Standards No. 158, “Employers’ Accounting for Defined Benefit

Pension and Other Postretirement Plans, an amendment of FASB

Statements No. 87, 88, 106, and 132(R)” (SFAS No. 158). SFAS No. 158

requires companies to recognize the overfunded or underfunded

status of a defined benefit postretirement plan as an asset or liabil-

ity in its consolidated balance sheet and to recognize changes in

funded status in the year in which the changes occur through other

comprehensive income. This standard also requires companies to

measure the funded status of a plan as of the date of its annual

consolidated balance sheet, with limited exceptions. SFAS No. 158

is effective for financial statements issued for fiscal years ending

after December 15, 2006; therefore, the Company expects to adopt

SFAS No. 158 at the end of fiscal 2007. Based on the information

Ty s on Foods, Inc. 2006 Annual Report29

Notes to Consolidated Financial Statements continued