Toyota 2009 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2009 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

The Right Way Forward Business OverviewPerformance Overview Financial Section

Investor

Information

Management &

Corporate Information

Top Messages

Annual Report 2009 59

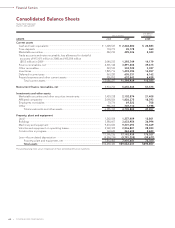

Related Party Transactions

Toyota does not have any significant related party transactions

other than transactions with affiliated companies in the ordinary

course of business. See note 12 to the consolidated financial

statements for further discussion.

Legislation Regarding End-of-Life Vehicles

In October 2000, the European Union enforced a directive that

requires member states to promulgate regulations implement-

ing the following:

• manufacturers shall bear all or a significant part of the costs for

taking back end-of-life vehicles put on the market after July 1,

2002 and dismantling and recycling those vehicles. Beginning

January 1, 2007, this requirement will also be applicable to

vehicles put on the market before July 1, 2002;

• manufacturers may not use certain hazardous materials in

vehicles sold after July 2003;

• vehicles type-approved and put on the market after December

15, 2008 shall be re-usable and/or recyclable to a minimum of

85% by weight per vehicle and shall be re-usable and/or

recoverable to a minimum of 95% by weight per vehicle; and

• end-of-life vehicles must meet actual re-use of 80% and re-use

as material or energy of 85%, respectively, of vehicle weight by

2006, rising to 85% and 95%, respectively, by 2015.

See note 23 to the consolidated financial statements for fur-

ther discussion.

Recent Accounting Pronouncements

in the United States

In December 2007, FASB issued FAS No. 141(R), Business

Combinations (“FAS 141(R)”). FAS 141(R) establishes principles

and requirements for how the acquirer recognizes and measures

the identifiable assets acquired, the liabilities assumed, any non-

controlling interest, and the goodwill acquired in a business

combination or a gain from a bargain purchase. Also, FAS 141(R)

provides several new disclosure requirements that enable users

of the financial statements to evaluate the nature and financial

effects of the business combination. FAS 141(R) is effective to

business combinations on and after the beginning of fiscal year

beginning on or after December 15, 2008. The impact of adopt-

ing FAS 141(R) on Toyota’s consolidated financial statements will

depend on the nature and significance of any acquisitions in the

future period.

In December 2007, FASB issued FAS No. 160, Noncontrolling

Interests in Consolidated Financial Statements—an amendment

of ARB No. 51 (“FAS 160”). FAS 160 amends the guidance in

Accounting Research Bulletins No. 51, Consolidated Financial

Statements, to establish accounting and reporting standards for

the noncontrolling interest in a subsidiary and for the deconsoli-

dation of a subsidiary. FAS 160 is effective for fiscal year, and

interim period within the fiscal year, beginning on or after

December 15, 2008. The presentation and disclosure require-

ments shall be applied retrospectively for all periods presented

in the consolidated financial statements in which FAS 160 is ini-

tially applied. Management is evaluating the impact of adopting

FAS 160 on Toyota’s consolidated financial statements.

In December 2008, FASB issued FASB Staff Position No. FAS

132(R)-1, Employers’ Disclosures about Postretirement Benefit

Plan Assets (“FSP FAS 132(R)-1”). FSP FAS 132(R)-1 requires

additional disclosures about postretirement benefit plan assets

including investment policies and strategies, categories of plan

assets, fair value measurements of plan assets, and significant

concentrations of risk. FSP FAS 132(R)-1 is effective for fiscal year

ending after December 15, 2009. Management does not expect

this Statement to have a material impact on Toyota’s consolidated

financial statements.

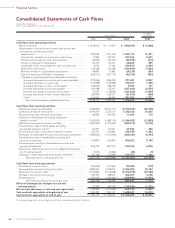

Toyota is unable to make reasonable estimates of the period of cash settlement with respect to liabilities recognized for uncertain tax

benefits, and accordingly such liabilities are excluded from the table above. See note 16 to the consolidated financial statements for fur-

ther discussion.

Toyota expects to contribute ¥95,270 million to its pension plans in fiscal 2010.

Yen in millions

Total Amount of Commitment Expiration Per Period

Amounts

Committed Less than 1 year 1 to 3 years 3 to 5 years 5 years and after

Commercial Commitments:

Maximum potential exposure to guarantees given

in the ordinary course of business (note 23) .................................. ¥1,570,497 ¥446,638 ¥724,503 ¥314,472 ¥84,884

Total Commercial Commitments .................................................. ¥1,570,497 ¥446,638 ¥724,503 ¥314,472 ¥84,884