Saks Fifth Avenue 2009 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2009 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

Table of Contents

SAKS INCORPORATED & SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(In thousands, except per share amounts)

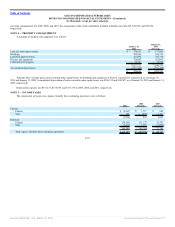

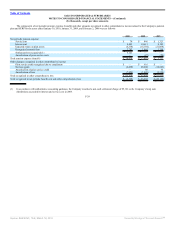

(for documentary or commercial letters of credit). The Company also pays an unused line fee ranging from 0.5% to 1.0% per annum on the average daily unused

revolver.

During periods in which availability under the agreement is $87,500 or more, the Company is not subject to financial covenants. If and when availability

under the agreement decreases to less than $87,500, the Company will be subject to a minimum fixed charge coverage ratio of 1 to 1. There is no debt rating

trigger.

The revolving credit agreement permits additional debt in specific categories including the following (each category being subject to limitations as

described in the revolving credit agreement): debt arising from permitted sale/leaseback transactions; debt to finance purchases of machinery, equipment, real

estate and other fixed assets; debt in connection with permitted acquisitions; and unsecured debt. The agreement also permits other debt (including permitted

sale/leaseback transactions) in an aggregate amount not to exceed $400,000 at any time, including secured debt, so long as it is a permitted lien as defined by the

revolving credit agreement. The revolving credit agreement also places certain restrictions on, among other things, asset sales, the ability to make acquisitions

and investments, and to pay dividends.

The Company routinely issues stand-by and documentary letters of credit principally related to the funding of insurance reserves. Outstanding letters of

credit reduce availability under the revolving line of credit. During 2009, weighted average letters of credit issued under the credit agreement were $25,734. The

highest amount of letters of credit outstanding under the agreement during 2009 was $52,455. At January 30, 2010, the Company had no direct outstanding

borrowings and had letters of credit outstanding of $28,525. The credit agreement contains default provisions that are typical for this type of financing, including

a provision that would trigger a default under the credit agreement if a default were to occur in another debt instrument resulting in the acceleration of principal

of more than $20,000 under that other instrument.

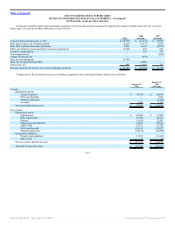

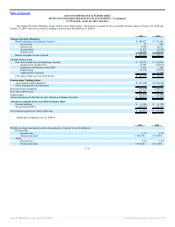

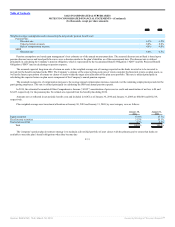

SENIOR NOTES

At January 30, 2010, the Company had $169,249 of unsecured senior notes outstanding, excluding the convertible notes, comprised four separate series

having maturities ranging from 2010 to 2019 and interest rates ranging from 7.00% to 9.88%. The senior notes are guaranteed by all of the subsidiaries that

guarantee the Company’s credit facility and have substantially identical terms except for the maturity dates and interest rates payable to investors. The notes

permit certain sale/leaseback transactions but place certain restrictions around the use of proceeds generated from a sale/leaseback transaction. The terms of each

senior note require all principal to be repaid at maturity. There are no financial covenants associated with these notes, and there are no debt-rating triggers.

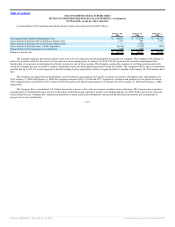

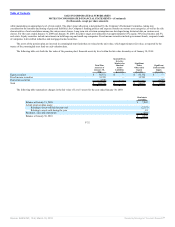

On April 12, 2007, the Company announced the results of its modified “Dutch Auction” tender offer to purchase a portion of its 8.25% senior notes due

November 15, 2008 for an aggregate purchase price not to exceed $100 million (the “offer cap”). The offer expired on April 11, 2007. The aggregate principal

amount of notes validly tendered at or above the clearing spread exceeded the offer cap and the Company accepted $95,872 aggregate principal amount of the

notes, resulting in an aggregate purchase price of approximately $100,000 (plus an additional $3,230 in aggregate accrued interest on such notes). The Company

accepted for purchase first, all notes tendered at spreads above the clearing spread, and thereafter, the notes validly tendered at the clearing spread on a prorated

basis according to the principal amount of such notes. During the three months ended May 5, 2007, the Company recorded a loss on extinguishment of debt of

approximately $5,222 related to the repurchase of the notes.

F-23

Source: SAKS INC, 10-K, March 18, 2010 Powered by Morningstar® Document Research℠