Radio Shack 2009 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2009 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

73

NOTE 11 – DERIVATIVE FINANCIAL INSTRUMENTS

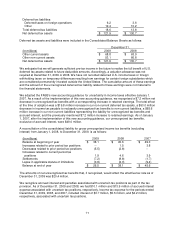

We enter into derivative instruments for risk management purposes only, including derivatives designated

as hedging instruments under the FASB’s accounting guidance on the accounting for derivative

instruments and hedging activities. We do not hold or issue derivative financial instruments for trading or

speculative purposes. To qualify for hedge accounting, derivatives must meet defined correlation and

effectiveness criteria, be designated as a hedge and result in cash flows and financial statement effects

that substantially offset those of the position being hedged.

By using these derivative instruments, we expose ourselves, from time to time, to credit risk and market

risk. Credit risk is the potential failure of the counterparty to perform under the terms of the derivative

contract. When the fair value of a derivative contract is positive, the counterparty owes us, which creates

credit risk for us. We minimize this credit risk by entering into transactions with high quality counterparties

and do not anticipate significant losses due to our counterparties’ nonperformance. Market risk is the

adverse effect on the value of a financial instrument that results from a change in the rate or value of the

underlying item being hedged. We minimize this market risk by establishing and monitoring internal

controls over our hedging activities, which include policies and procedures that limit the types and degree

of market risk that may be undertaken.

Interest Rate Swap Agreements: We use interest rate-related derivative instruments to manage our

exposure to fluctuations of interest rates. In June and August 2003, we entered into interest rate swap

agreements with underlying notional amounts of debt of $100 million and $50 million, respectively, and both

with maturities in May 2011. These swaps effectively convert a portion of our long-term fixed rate debt to a

variable rate. We entered into these agreements to balance our fixed versus floating rate debt portfolio to

continue to take advantage of lower short-term interest rates. Under these agreements, we have contracted

to pay a variable rate of LIBOR plus a markup and to receive fixed rates of 7.375%.

The swap agreements were originally designated as fair value hedges of the related debt and met the

requirements to be accounted for under the short-cut method, resulting in no ineffectiveness in the hedging

relationship. The periodic interest settlements, which occur at the same interval as the interest payments on

the 2011 Notes, are recorded as interest expense. The gain or loss on these derivatives, as well as the

offsetting loss or gain on the related debt, was recognized in current earnings, but had a net earnings

effect of zero due to short-cut method accounting.

In September 2009, we repurchased $43.2 million of our 7.375% unsecured notes due in 2011. A portion of

these notes were hedged by our interest rate swaps. Upon repurchase of these notes, we were required to

discontinue the hedge accounting treatment associated with these derivative instruments which used the

short-cut method. We intend to hold these instruments until their maturities. Changes in fair value of these

instruments are recorded in earnings as an adjustment to interest expense.