Radio Shack 2009 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2009 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

33

On October 20, 2009, Fitch updated our rating outlook to stable from negative. Other than the change in

Fitch’s outlook, these ratings are consistent with the ratings and outlooks reported in our Annual Report

on Form 10-K for the year ended December 31, 2008. Factors that could affect our future credit ratings

include free cash flow and cash levels, changes in our operating performance, the adoption of a more

aggressive financial strategy, the economic environment, conditions in the retail and consumer

electronics industries, sales declines in comparable stores, our financial position and changes in our

business strategy. If downgrades occur, which we do not expect, they will adversely affect our future

borrowing costs, access to debt capital markets, vendor financing terms and future new store occupancy

costs.

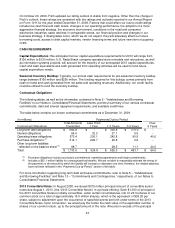

CASH REQUIREMENTS

Capital Expenditures: We anticipate that our capital expenditure requirements for 2010 will range from

$100 million to $120 million. U.S. RadioShack company-operated store remodels and relocations, as well

as information systems projects, will account for the majority of our anticipated 2010 capital expenditures.

Cash and cash equivalents and cash generated from operating activities will be used to fund future

capital expenditure needs.

Seasonal Inventory Buildup: Typically, our annual cash requirements for pre-seasonal inventory buildup

range between $150 million and $250 million. The funding required for this buildup comes primarily from

cash on hand and cash generated from net sales and operating revenues. Additionally, our credit facility

could be utilized to fund the inventory buildup.

Contractual Obligations

The following tables, as well as the information contained in Note 5 - "Indebtedness and Borrowing

Facilities" to our Notes to Consolidated Financial Statements, provide a summary of our various contractual

commitments, debt and interest repayment requirements, and available credit lines.

The table below contains our known contractual commitments as of December 31, 2009.

(In millions) Payments Due by Period

Contractual Obligations

Total Amounts

Committed

Less Than

1 Year

1-3 Years

3-5 Years

Over

5 Years

Long-term debt obligations $ 682.8 $ -- $ 306.8 $ 376.0 $ --

Interest obligations 64.6 32.0 27.1 5.5 --

Operating lease obligations 573.4 200.1 242.8 90.5 40.0

Purchase obligations (1) 314.1 292.7 20.8 0.6 --

Other long-term liabilities

reflected on the balance sheet (2)

98.7

28.5

11.1

24.0

Total $ 1,733.6 $ 524.8 $ 626.0 $ 483.7 $ 64.0

(1) Purchase obligations include our product commitments, marketing agreements and freight commitments.

(2) Includes a $35.1 million liability for unrecognized tax benefits. We are not able to reasonably estimate the timing of

the payments or the amount by which the liability will increase or decrease over time; therefore, the related balances

have not been reflected in the ‘‘Payments Due by Period’’ section of the table.

For more information regarding long-term debt and lease commitments, refer to Note 5 – “Indebtedness

and Borrowing Facilities” and Note 13 – “Commitments and Contingencies,” respectively, of our Notes to

Consolidated Financial Statements.

2013 Convertible Notes: In August 2008, we issued $375 million principal amount of convertible senior

notes due August 1, 2013, (the “2013 Convertible Notes”) in a private offering. Each $1,000 of principal of

the 2013 Convertible Notes is initially convertible, under certain circumstances, into 41.2414 shares of our

common stock (or a total of approximately 15.5 million shares), which is the equivalent of $24.25 per

share, subject to adjustment upon the occurrence of specified events set forth under terms of the 2013

Convertible Notes. Upon conversion, we would pay the holder the cash value of the applicable number of

shares of our common stock, up to the principal amount of the note. Amounts in excess of the principal