Radio Shack 2009 Annual Report Download - page 16

Download and view the complete annual report

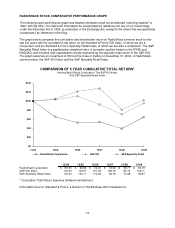

Please find page 16 of the 2009 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

9

Any reductions or changes in the growth rate of the wireless industry or changes in the dynamics

of the wireless communications industry could materially adversely affect our results of

operations.

Sales of wireless handsets and the related commissions and residual income constitute a significant

portion of our total revenue. Consequently, changes in the wireless industry, such as those discussed

below, could materially adversely affect our results of operations and financial condition.

Lack of growth in the overall wireless industry tends to have a corresponding effect on our wireless sales.

Because growth in the wireless industry is often driven by the adoption rate of new wireless handset and

wireless service technologies, the absence of these new technologies, our suppliers not providing us with

these new technologies, or the lack of consumer interest in adopting these new technologies, could

adversely affect our business.

Another change in the wireless industry that could materially adversely affect our profitability is wireless

industry consolidation. Consolidation in the wireless industry could lead to a concentration of competitive

strength within a few wireless carriers, which could adversely affect our business if our ability to obtain

competitive offerings from our wireless suppliers is reduced or as competition from wireless carrier stores

increases.

Our competition is both intense and varied, and our failure to effectively compete could materially

adversely affect our results of operations.

In the retail consumer electronics marketplace, the level of competition is intense. We compete with

consumer electronics retail stores similarly situated to our stores as well as big-box retailers, large

specialty retailers and discount or warehouse retailers and, to a lesser extent, with alternative channels of

distribution such as e-commerce, telephone shopping services and mail order. We also compete with

wireless carriers’ retail presence, as discussed above. Some of these other competitors are larger than us

and have greater market presence and financial and other resources than us, which may provide them

with a competitive advantage.

Changes in the amount and degree of promotional intensity or merchandising strategy exerted by our

current competitors and potential new competition could present us with difficulties in retaining existing

customers and attracting new customers. In addition, pressure from our competitors could require us to

reduce prices or increase our costs in one product category or across all our product categories. As a

result of this competition, we may experience lower sales, margins or profitability, which could materially

adversely affect our results of operations.

In addition, some of our competitors may use strategies such as lower pricing, wider selection of

products, larger store size, higher advertising intensity, improved store design, and more efficient sales

methods. While we attempt to differentiate ourselves from our competitors by focusing on the electronics

specialty retail market, our business model may not enable us to compete successfully against existing

and future competitors.

We may not be able to maintain our historical gross margin levels.

Historically, we have maintained gross margin levels ranging from 45% to 48%. We may not be able to

maintain these margin levels in the future due to various factors, including increased sales of lower

margin products, such as personal electronics products and name brand products, or declines in average

selling prices of key products. If sales of lower margin items continue to increase and become a larger

percentage of our business, our gross margin will be adversely affected.